February 28, 2023

Introduction:

Over the past decade, the field of cryptocurrency has seen a dramatic expansion in our financial system. One of the areas that has seen the greatest change in this regard is the area of investing. Cryptocurrency now represents a major area of investment, with millions of people choosing to invest in a number of different cryptocurrencies. Until recently, this was a major growth area; in fact, the 2022 football Super Bowl was nicknamed the “Crypto Bowl,” because so many of the major ads for that contest were sponsored by various cryptocurrency exchanges. However, 2022 saw a dramatic drop in the value of Bitcoin, currently one of the dominant cryptocurrency tokens; the recent volatility of cryptocurrency was exacerbated by the collapse of the FTX cryptocurrency exchange, but Bitcoin has seen strong devaluations periodically since its introduction in 2009.

In this post, we will review the field of cryptocurrency. In Part I of this post, we will discuss the motivation behind the development of cryptocurrency, and we will review the philosophy espoused by the founders of this financial system, a group who called themselves the Cypherpunks. We will provide some details about individuals who have been prominent in the development of cryptocurrency and cryptocurrency exchanges. Next, we will discuss the mechanics of the Bitcoin blockchain, the essentially incorruptible record, stored on many worldwide computers, of all transactions carried out with Bitcoin since its inception. The blockchain is one of the technical aspects of a financial system which operates without any of the physical structures, personnel, or government-supplied insurance that characterize the traditional banking and finance systems. We will focus on the Bitcoin blockchain and Bitcoin “mining,” since up to the present (Feb. 2023) Bitcoin has been the most widely held cryptocurrency. However, we will also discuss the Ethereum currency, since the ‘smart contracts’ introduced by Ethereum have the potential of greatly expanding the types of financial transactions carried out using blockchain technology.

One of the initial claims was that blockchain technology would guarantee the privacy of users of the system, since those users could only be deciphered with the use of a ‘private cryptographic key,’ which was available only to the individual user. However, this has not turned out to be the case. In Part II, we show how it has become possible to identify users and transactions even without access to a private key. We will discuss the development of techniques to trace individual transactions on the blockchain; and we will trace the rise of Chainalysis, the largest company that attempts to analyze blockchain interactions. Because of its ability to identify individuals who engage in financial transactions on the blockchain, Chainalysis has become very popular with government departments that track illegal activities that use cryptocurrency. We will review how multinational agencies using Chainalysis tracing methods were able to take down two of the larger Dark Web anonymous markets: the Silk Road Dark Web site that specialized in the illegal drug trade, and the Welcome to Video site that assembled videos showing child sexual abuse, which users were able to access using cryptocurrency.

In part III of this post we will address the question of whether cryptocurrencies are fulfilling their promise of providing an alternative to traditional financial systems, completely independent of banks and governments? A viable financial system should be stable, secure and should represent a system that is more or less universally accepted for financial transactions. We will show that, at least at present, cryptocurrencies have not managed to provide stability, security or widespread acceptance. Furthermore, the continuing use of cryptocurrencies for illicit activities, including the Dark Web, scams and outright theft, has begun to attract significant regulation of the cryptocurrency industry, so that it will no longer be quite so independent of governments. We will conclude with some speculation about the future of cryptocurrency.

Section I: Some Founders of the Cryptocurrency System:

The founding fathers of Bitcoin come from a group of people who were referred to as Cypherpunks. These were individuals who were interested in achieving privacy and security through the proactive use of cryptography. This was a movement that originated in the late 1980s. Before that time, cryptography was mainly limited to the military and spy agencies such as the U.S. National Security Agency. However, in 1976 the National Bureau of Standards published the Data Encryption Standard algorithm for encrypting digital data. Later that year Diffie and Hellman published a seminal paper on public-key cryptography. This motivated computer scientists to develop systems of banking that might do away with the role of banks as third parties in financial transactions.

A group of computer scientists meeting in San Francisco were named ‘Cypherpunks’, a portmanteau word that combines ‘ciphers’ with ‘cyberpunks.’ A Cypherpunk mailing list was created in 1992 and by 1997 was estimated to include 2,000 subscribers. E-mails exchanged on this list ranged from mathematics, cryptography and computer science to political and philosophical discussions. The aims of this group were outlined in Eric Hughes’ 1993 publication A Cypherpunk’s Manifesto. “Privacy is necessary for an open society in the electronic age … We cannot expect governments, corporations or other large, faceless organizations to grant us privacy … We must defend our own privacy if we expect to have any … Cypherpunks write code. We know that someone has to write software to defend privacy, and … we’re going to write it.” Steven Levy described the process by which cryptography tools were used to protect individual privacy as one where “The tools of prying are transformed into the instruments of privacy.”

The Cypherpunks included people with a great variety of personal philosophies. Although all of them were concerned with maintaining the privacy of individuals and were fascinated by the role of cryptographic techniques in securing privacy, they disagreed on the aims and aspirations of this movement. In some cases, the Cypherpunks were interested in freedom from government collection of information about its citizens. Many of the Cypherpunks felt that their contributions might be extremely useful for people living in repressive states. For example, citizens in countries such as North Korea, China, or Iran might welcome technologies that would allow them to communicate freely without fear of reprisals. And the libertarian instincts of the Cypherpunks made them sympathetic to people who wanted to prevent the government from accessing their financial information or spying on their political activities.

More radical Cypherpunks were what might be termed “privacy absolutists.” These people were convinced that protection of individual privacy was an absolute right that must be protected regardless of the uses of their technology. These individuals would even condone the use of cryptographic techniques for illegal activities such as drug dealing, child sexual abuse or human trafficking. The argument was that tolerating these activities was a necessary part of guarding individual privacy. And they also argued that governments could use other techniques for combating crime without resorting to warrantless surveillance of citizens. This sets up a tension between privacy concerns and anti-crime initiatives. Later in this post we will discuss efforts by authorities to curb illegal activities that might be facilitated by the use of cryptographic technology.

One of the most succinct statements of the philosophy of the ‘privacy absolutists’ was provided by Timothy May, in his 1988 proclamation, The Crypto Anarchist Manifesto: “The State will of course try to slow or halt the spread of [encryption] technology, citing national security concerns, use of the technology by drug dealers and tax evaders, and fears of societal disintegration. Many of these concerns will be valid: crypto anarchy will allow national secrets to be traded freely and will allow illicit and stolen materials to be traded. An anonymous computerized market will even make possible abhorrent markets for assassinations and extortion. Various criminal and foreign elements will be active users of CryptoNet. But this will not halt the spread of crypto anarchy.”

Next, we will discuss a few individuals who have been prominently associated with the rise of cryptocurrency.

Satoshi Nakamoto:

Any discussion of cryptocurrency must begin with Satoshi Nakamoto. On August 18, 2008 Satoshi Nakamoto registered the domain name bitcoin.org. On Oct. 31, 2008 Nakamoto wrote the first white paper “Bitcoin: A Peer-to-Peer Electronic Cash System” that described a digital cryptocurrency. This paper was uploaded to the cryptography mailing list at the domain metzdowd.com. On Jan. 9, 2009 Nakamoto released the first version of the Bitcoin software. Nakamoto continued to be heavily involved in the early development of Bitcoin; and he produced the first blockchain database. Until December 2010, Nakamoto was quite active in the early days of cryptocurrency.

Unfortunately, ‘Satoshi Nakamoto’ appears to be a pseudonym. There have been many attempts to discover his identity (although Nakamoto’s gender is not known, we will refer to “him” since Satoshi is a male Japanese name). For a start, people would like to know who published the original idea for Bitcoin, and would like to interview him (alternatively, ‘Nakamoto’ may refer to a group of anonymous software developers). Another reason for interest in finding Satoshi Nakamoto is that, as part of the development of Bitcoin procedures, Nakamoto took part in early data-mining efforts. As a result, he amassed roughly 1 million Bitcoins. At its current value (Feb. 2023) of roughly $20,000 per Bitcoin, Nakamoto would be holding about $20 billion in Bitcoin. However, the Bitcoin have been sitting in Nakamoto’s account for the past dozen years, without any of it being redeemed.

In March, 2014 reporter Leah McGrath Goodman published a cover-page article claiming to have identified Satoshi Nakamoto. The cover of that issue of Newsweek is shown in Figure I.1. Goodman claimed that the Bitcoin developer was Dorian Satoshi Nakamoto, a physicist and systems engineer in Southern California. However, Nakamoto denied that he had been involved in the development of Bitcoin.

Figure I.1: The March 2014 cover of Newsweek magazine. An article titled ‘Bitcoin’s Face’ claimed to have discovered the founder of Bitcoin, and it named Southern California Japanese-American Dorian Satoshi Nakamoto as the originator of that cryptocurrency. Nakamoto denied that he was involved in the development of Bitcoin.

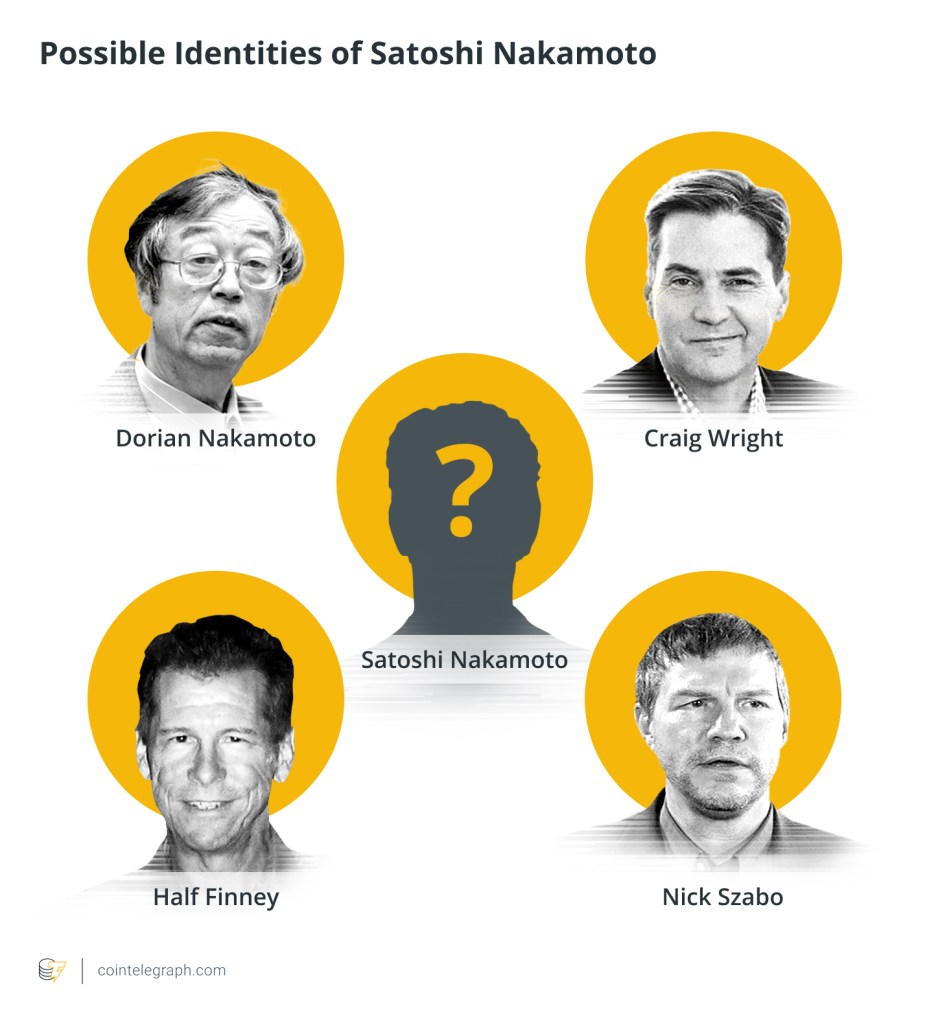

Following the Newsweek article, several others have been suggested as being Nakamoto. These are individuals who were active in the financial sector work of cypherpunks. Figure I.2 shows four of these, including Dorian Nakamoto. The remaining three are Nick Szabo, Hal Finney and Craig Wright. Nick Szabo is a computer scientist and lawyer who has made many contributions to cryptography. In 1998 Szabo wrote about a mechanism for producing a digital decentralized currency he called “bit gold.” Although Szabo’s idea never materialized, it is considered a precursor to Bitcoin. Szabo also developed the idea of ‘smart contracts.’ These were automated and secure business functions that could be created without third-party intermediaries (this will be discussed in our section on Ethereum). Szabo denies that he is Satoshi Nakamoto.

Figure I.2: Four individuals who have been suggested as being Satoshi Nakamoto, the author of the first whitepaper describing Bitcoin, creator of the first source code for Bitcoin, and an early active individual in Bitcoin transactions. Clockwise from upper left: Dorian Sakamoto; Craig Wright; Nick Szabo; and Hal Finney.

Hal Finney was an American software developer. In 2004, Finney created the first automated ‘proof-of-work’ system. This became an important feature of the Bitcoin system, providing a mechanism for the issuance (or “mining”) of new Bitcoins and an inducement for honest worldwide competition to add verifiable blocks to the blockchain. In addition, Finney was the recipient of the first Bitcoin network transaction, where he received a payment in Bitcoin from Satoshi Nakamoto. The fourth major suspect of being Satoshi Nakamoto was Craig Wright. Wright is an Australian computer scientist who currently lives in the U.K. Wright was active in the creation of an online casino in Australia, and he was also the CEO of the company Preemptive Intelligence Group that planned to open a bank that utilized Bitcoin as currency. In 2015, a couple of articles appeared that claimed Wright was “Satoshi Nakamoto.” Wright encouraged this speculation, although several scientists in the crypto community claimed that he was engaged in a massive fraud. At one point, Wright claimed that he was the leader of a group that included Hal Finney and Dave Kleiman, and that the three of them had collaborated as “Satoshi Nakamoto.” In February 2018 the estate of Dave Kleiman sued Wright. It claimed that Kleiman and Wright had mined Bitcoin from 2009 to 2018 and claimed that Wright had defrauded Kleiman of over $5 billion in Bitcoin. The judge in the lawsuit awarded Kleiman’s estate $100 million in damages, and the judge stated that “Dr. Wright’s story not only was not supported by other evidence in the record, it defies common sense and real-life experience.”

Sam Bankman-Fried:

Sam Bankman-Fried is the son of two Stanford University law professors, Joseph Bankman and Barbara Fried. He graduated from MIT in 2014 with a degree in physics and a minor in math. Bankman-Fried then worked at the Center for Effective Altruism (CEA, now known as Effective Altruism). This was an organization founded by two philosophers at Oxford University. Its goal is to build a community of people who are mindful of the world’s greatest problems and who take action to solve those problems with the aid of financial resources provided by altruists. Bankman-Fried was the director of development for CEA for a short time in 2017; he left that organization to create the quantitative trading firm Alameda Research. In April 2019, Bankman-Fried formed the cryptocurrency derivatives exchange FTX.

Figure I.3: Sam Bankman-Fried. He was the founder of the trading firm Alameda Research and the cryptocurrency exchange firm FTX. For a while, FTX appeared to be the most profitable cryptocurrency exchange. However, after a crash in November 2022, FTX declared bankruptcy.

For a while, FTX appeared to be a stunning success. Bankman-Fried enlisted a number of high-profile figures in the world of entertainment and sports as spokespersons for FTX. These included Tom Brady and his then-wife Gisele Bundchen, Stephen Curry, Naomi Osaka, Shohei Ohtani, Shaquille O’Neal, Trevor Lawrence and Larry David. FTX took out multi-page ads in magazines such as The New Yorker, and he paid $135 million for naming rights to the arena for the Miami Heat (it was then called FTX Arena), and another $30 million for a single ad during the 2022 Super Bowl. At age 25 in 2017, Bankman-Fried was the youngest self-made billionaire. In 2021, Bankman-Fried’s net worth was estimated at $26 billion, which made him the 41st richest American and the 60th richest person in the world. Bankman-Fried stated that his mission was to pursue “earning to give” as part of his commitment to the Effective Altruism movement. At various times, he made lofty statements regarding his charitable intentions.

However, in November 2022 Bankman-Fried became involved in a feud with Changpeng Zhao, the CEO of a rival cryptocurrency company Binance. At the beginning of that month, Zhao issued a message on Twitter that Binance intended to sell all of its holdings of FTT, which was the currency token for FTX. Since Binance held massive amounts of FTT, and the trading volume for that currency was small, the value of FTT crashed. The Bloomberg Billionaires Index reported that Bankman-Fried’s net worth had declined by 94% in one day. On November 8, 2022, Zhao announced that Binance intended to purchase FTX. The following day, Zhao reported that, because of reports that FTX had mishandled customer funds and that FTX was being investigated for potential criminal acts, Binance would not be purchasing FTX. Two days later, FTX declared bankruptcy. On Nov. 11, Bankman-Fried stepped down as CEO of FTX. He was replaced by John Ray, who had taken on a similar role in the bankruptcy of Enron.

In Dec. 2022, John Ray testified before the U.S. House Financial Services Committee regarding his evaluation of the financial system at FTX. Ray testified that Alameda Research had received customer funds from FTX. “Funds from FTX.com … were used at Alameda to make investments and other disbursements,” testified Ray. Ray continued, “Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here … literally there’s no record keeping whatsoever.” These are strong words from the man who was charged with overseeing the bankruptcy proceedings of Enron.

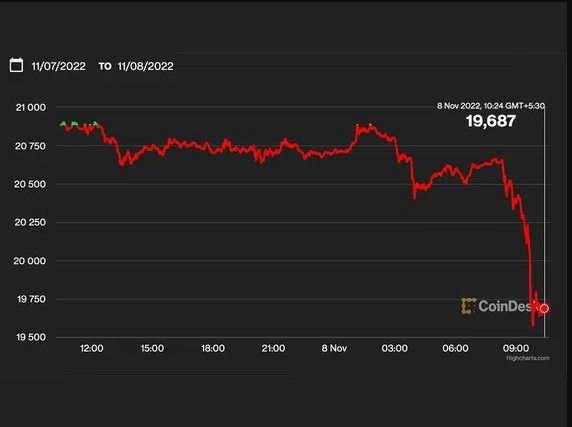

Shortly afterwards, various news sources revealed that in 2022, Sam Bankman-Fried had transferred more than $4 billion from FTX accounts to Alameda Research, without notifying any of the officers of FTX of his actions. Sources within FTX reported that Alameda Research owed FTX $10 billion. In a matter of days, Bankman-Fried’s reputation turned from ‘boy wonder’ to ‘fraudster.’ On Dec. 12, 2022 Sam Bankman-Fried was arrested at his home in the Bahamas and was subsequently extradited to the U.S. He was charged with a number of criminal offenses, including “wire fraud, commodities fraud, securities fraud, money laundering and campaign finance law violations.” Although Bankman-Fried denied that he had committed these offenses and insisted that FTX had far more resources than regulators alleged, a number of his colleagues at FTX and Alameda Research have pleaded guilty and are cooperating with the authorities. If convicted on all of the counts against him, Sam Bankman-Fried could be sentenced to as many as 115 years in prison. The collapse of FTX caused a dramatic devaluation of all cryptocurrencies not fixed to the US dollar or other stable resource, as illustrated in Fig. I.4 by the hour-by-hour value of Bitcoin from Nov. 7 to 8, 2022.

Figure I.4. The impact of the FTX collapse on Bitcoin’s trading value on Nov. 8, 2022.

Changpeng Zhao:

Changpeng Zhao is the founder of the cryptocurrency exchange Binance. He is a Chinese-Canadian citizen who currently operates out of Singapore. Zhao graduated from McGill University with a degree in computer science. In 2005, Zhao moved to Shanghai and founded Fusion Systems, a firm that specialized in ultra-high-frequency commodities trading. In 2014, Zhao sold his house and used the proceeds to invest in Bitcoin. Zhao has announced that 100% of his wealth is invested in cryptocurrency. He has also announced his intent to eventually donate up to 99% of his wealth to charity.

Figure I.5: Changpeng Zhao, founder of the Binance cryptocurrency exchange. By April 2018, Binance had become the world’s largest cryptocurrency exchange by trading volume. In Nov. 2022, Zhao announced that Binance was selling off all of its holdings of FTT, the currency token for FTX. This caused the immediate collapse and bankruptcy of FTX.

In July 2017, Zhao launched the Binance cryptocurrency exchange. This became an overnight success, and by April 2018 Binance had the largest trading volume of any cryptocurrency exchange. In April 2019 Binance introduced Binance Smart Chain. This enabled Binance to execute smart contracts, which made Zhao’s firm a major competitor to Ethereum. And in 2022, Binance invested $500 million to help finance Elon Musk’s acquisition of Twitter. In Nov. 2022, Zhao became embroiled in a disagreement with Sam Bankman-Fried’s FTX. He announced that Binance would divest itself of all its holdings in FTT, the currency token of FTX. The resulting publicity caused FTX to crash and declare bankruptcy; at this time, it was revealed that FTX had apparently been involved in illegal dealings, with FTX customer funds being transferred to shore up the trading firm Alameda Research. In addition, it was revealed that FTX had loaned its CEO Bankman-Fried $1 billion. John Ray, who is tasked with winding up the finances of FTX, reported that in at least one transaction Sam Bankman-Fried had signed as both the maker of a loan and as the recipient of the same loan.

Section II: Cryptography and the Bitcoin Blockchain:

Cryptocurrency technology revolves around the use of cryptographic techniques to maintain both the privacy of those involved in financial transactions and the security of its publicly available transaction ledger. It is also essential to the creation of a system that is designed to allow a number of financial and legal transactions to take place in the absence of bankers or lawyers, and banks or law firms. Here we will briefly outline the features of cryptography that are used in establishing cryptocurrency exchanges. At present, Bitcoin is the cryptocurrency with the largest market capitalization; so we will describe how the Bitcoin cryptocurrency system operates. In discussing cryptographic techniques and blockchain technology, we have made use of the book The Basics of Bitcoins and Blockchains: An Introduction to Cryptocurrencies and the Technology That Powers Them, by Antony Lewis.

Cryptography involves the acts by which information is encrypted (changed using a particular algorithm) and decrypted (converted back into the original information). A simple example would be what is called symmetric cryptography. In this case, the same algorithm is used to encrypt and then decrypt the information. Consider a message being sent from Alice to Bob: “How are you doing?” We encrypt this using a letter-substitution algorithm: in the encrypted version, each letter is replaced by the next letter in the alphabet. The encrypted message would be “Ipx bsf zpv epjoh?” When Bob receives the message he applies the same letter substitution, but in the reverse order, to obtain the decrypted message “How are you doing?” The encryption process is symmetric because the same algorithm is used to encrypt and (in reverse) to decrypt the message.

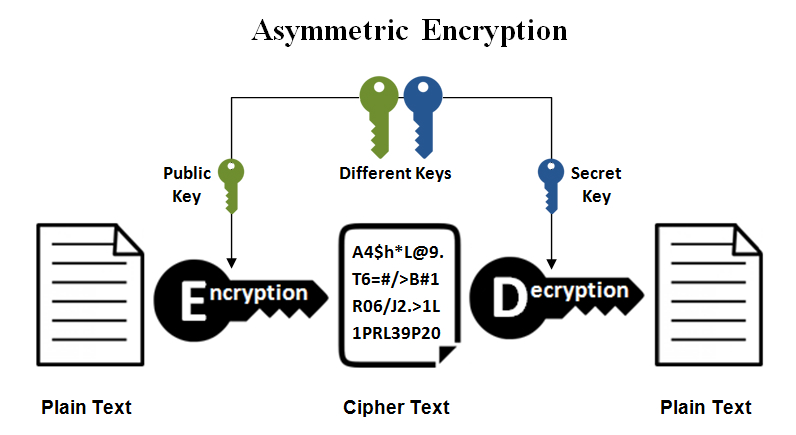

Symmetric cryptography is not used in blockchain technology, for several reasons. First, it requires that Bob and Alice communicate beforehand to agree on the algorithm to be used. Second, the encrypted message can be decrypted by anyone who can figure out the algorithm that was used to encrypt the message. Blockchain methods use what is called asymmetric cryptography. This is shown schematically in Figure II.1. The sender encrypts a message using a public key. The encrypted message is then sent to the recipient, who has a private key that is mathematically related to the public key. Using the private key, the recipient is able to decrypt the message. Without the private key, the message cannot be deciphered, and at present it is not possible to deduce the private key from the public key.

Figure II.1: A schematic depiction of asymmetric encryption. The original message is encrypted using a public key. The message is then sent to the recipient, who has a private key that is mathematically related to the public key. The recipient uses the private key to decrypt the message.

Bitcoin uses a method for determining the private key that is called Elliptic Curve Digital Signal Algorithm, or ECDSA. With this technique, you generate a random number between 1 and 2256– 1. This produces a number with 78 decimal digits, and that number is the private key. Given the private key, one performs some ECDSA mathematics to generate a public key. However, given the public key only, there is no way at present to deduce the private key.

The next quantity used in blockchain techniques is called the hash function. A hash function is a set of steps that can be applied to input data that produces a certain outcome, which is called the hash (alternatively the output can be called a fingerprint or a digest). Let us return to our original message “How are you doing?” We choose an algorithm where the hash is the first letter of the message. Using this rule, the hash for our message is “H”. This particular rule is known as a basic hash function. In cryptography, the algorithms used for hash functions have particular useful properties. Hash functions that are useful for cryptographic purposes have five desirable characteristics:

- The hash is deterministic (the identical input always produces the same hash)

- For any given message, you can quickly compute its hash

- You can’t ‘work backwards’ (deduce the message by knowing the hash)

- A small change in the message should produce a big change in the hash

- It is not feasible for two different messages to have the same hash

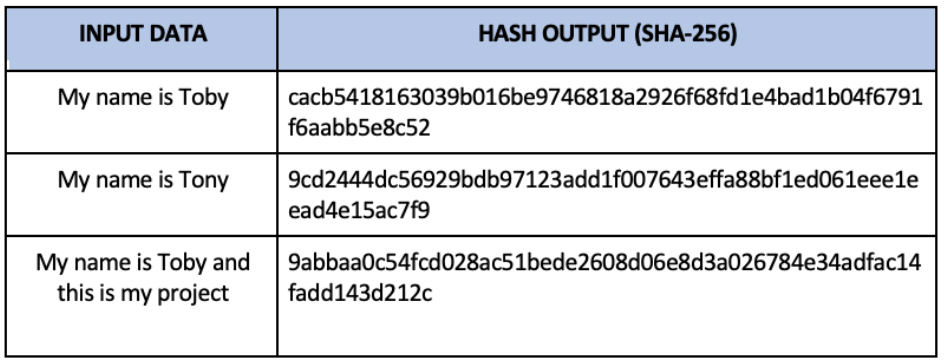

With these characteristics, the only way that you can deduce the message by knowing the hash is to try all possible messages until you obtain the same hash value. Obviously, the simple algorithm we introduced in the previous paragraph (the hash = first letter of the message) does not satisfy the fourth requirement for a good cryptographic hash, since any message that has the same first letter would produce the same hash value. There are a number of hash functions that are widely used in cryptography. Figure II.2 shows the results using the Secure Hash Algorithm 256-bit, or SHA-256, for three different inputs. SHA-256 converts any input to a unique 256-bit binary number, which can also be represented by a 64-digit hexadecimal number, where each digit is represented by a number between 0 and 9 or a letter between A and F. In the example in Fig. II.2, first, changing just a single letter in the message radically changes the output hash function. Also, the hash value for each message has the same length, regardless of the length of the message itself. This feature is very useful when constructing the blockchain. Cryptographic hashes are widely used in blockchain technology.

Figure II.2: The cryptographic hash function SHA-256 applied to three different messages. The first message is “My name is Toby.” The second is “My name is Tony.” The third message is “My name is Toby and this is my project.” To the right of each message is printed the hash output using SHA-256.

Next we discuss the use of ‘digital signatures’ on documents. At the end of a message, you apply a mathematical formula using your private key. This generates a digital signature. Anyone who sees your message and who knows the public key can verify that it was validated by you. The digital signature replaces a handwritten signature, which could be forged by anyone who had seen your signature. And the signature applies only to the accompanying message; so, you could not ‘go back’ and change or append the digital signature at some later time.

The Bitcoin Blockchain:

A set of rules for the Bitcoin blockchain was outlined in a whitepaper published in October 2008 by the pseudonymous Satoshi Nakamoto, who was profiled in the preceding Section. He envisioned creating a system of electronic cash, that “would allow payments to be sent directly from one party to another without going through a financial institution.” In order to create such a system, one needs to produce a method for transactions that is completely automated. In the traditional banking system, you have a bank vault that holds your money, plus tellers who verify your identity, check the status of your account, and process your request. In addition, accountants keep the books and register all transactions. The bank administration guarantees that the banking rules are being followed. The digital transaction network is designed as a system that operates and validates itself in the absence of third parties. So here is a summary of the Bitcoin system that was inspired by Nakamoto’s nine-page paper, based on the use of cryptographic techniques to ensure anonymity of the users and inviolability of the blockchain.

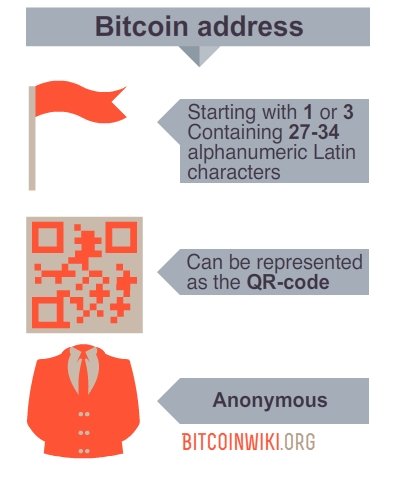

The first thing we do is to replace your bank account information by digital equivalents. Your account number is replaced by your public key, and your signature is replaced by your digital signature. With the Bitcoin system, you use your public key to generate a “wallet” address, and this is what is used as your identification (one individual may use many distinct wallets for different transactions). Figure II.3 gives a schematic picture of the generation of a Bitcoin address. Using your private key, you generate a public key, and a mathematical operation on that public key produces a Bitcoin address that is between 27 and 34 characters long. From that Bitcoin address you can also generate a QR code that can be used in transactions. By performing different operations on your private key, you can generate any number of accounts and use them for transactions.

Figure II.3: Generation of a Bitcoin address, the digital equivalent of your bank account number. The digital address can be converted into a QR code, and that code can be used in transactions.

The good news is that the system is designed to protect your anonymity (or, more precisely, pseudonymity, since the private key is your pseudonym). By doing away with the bank personnel, in theory no one knows who you are on the blockchain. In addition, if you are borrowing funds, you do not have to submit to a credit check, since you are anonymous. However, in doing away with banks, you have also made yourself vulnerable in other ways. First, if you forget your private keys or your Bitcoin wallet addresses, your assets are lost. (At the moment, nearly 4 million Bitcoins out of a maximum eventual supply of 21 million appear from Chainalysis accounting to be lost!) There is no way that you can retrieve a lost private key. Equally bad, if someone is able to steal your private key, they can impersonate you on the blockchain and transfer your assets to their own account. There is currently no “Federal Deposit Insurance Corporation” that guarantees the protection of your assets. And there is a thriving business in stealing private keys from individuals. Because the private keys are long strings of letters and numbers that are extremely difficult to memorize, people make and keep lists of their private keys. If users keep a list of their private keys on their computers, hackers will search through unsecured databases to find and steal private keys.

Next, we want to eliminate the role of “bookkeeper,” the person who maintains the ledger of accounts at a bank. The way this is done is to create a system where anyone can be the bookkeeper, but all who engage in bookkeeping get to verify the accuracy of the books. A record of all transactions is maintained on a gigantic public ledger – this ledger is the Bitcoin blockchain. It keeps a record of all transactions ever carried out on its public key, and this record is visible to all. Furthermore, the system is designed so that people cannot go back and alter the ledger, so that hackers cannot later transfer assets back to their own accounts, or ‘double-pay’ (use the same Bitcoin twice in transactions). And this ‘ledger’ or Bitcoin blockchain is maintained and updated on many different computers worldwide.

The idea of the ledger being stored on multiple computers and updated regularly immediately raises an issue. Imagine that a million Bitcoin transactions are executed every day. If every user individually uploaded the result of their transaction, it would become nearly impossible for all the computers that stored the ledger to keep track of the order of the transactions. Furthermore, it would become equally difficult for all servers to update these transactions ‘in chronological order.’

Cryptocurrency networks deal with the issue of adding information to the system. In the Bitcoin system a pair of users performs a transaction, and they offer a ‘transaction fee’ to a bookkeeper who collects a batch of different transactions into a single ‘block.’ In principle, anyone could be a bookkeeper. A single block includes a large number of transactions, in Bitcoin’s case as many transactions as occur worldwide in each 10-minute period, and when the block is accepted it will be added to all previously existing blocks. The blockchain is the sum of all blocks that have been added in chronological order. So, the blockchain grows in length as each block is added to the chain. Each new block has a unique identifying cryptographic hash that is generated in a competitive fashion described below, incorporating information from the transactions in the new block as well as from the identifying hash of the preceding block. This dependence on information in the preceding block serves as the link in the unbroken chain; in order to maintain self-consistency a would-be hacker attempting to alter the blockchain after the fact would have to regenerate the entire blockchain following the block the hacker wants to alter, and that would require so much computational resources as to make the hack unprofitable. This is how security is built into the blockchain. If all the computer nodes keeping track of the ledger verify and accept the new block, it is ‘integrated’ into the system and the blockchain is updated on all nodes.

Figure II.4: How transactions are entered into the bookkeeping network. A bunch of individual transactions are bundled together into a ‘block’ of transactions. Each user offers a transaction fee to the person who assembles the block.

Bitcoin Mining:

An individual transaction is considered ‘pending’ until it has been successfully loaded onto a block, and that block has been added to the blockchain. A given blockchain system has a built-in mechanism to ensure that new blocks are added at regular intervals. For example, the Bitcoin blockchain automatically adjusts so that one new block is added every 10 minutes. How is this accomplished? Bitcoin holds a competition among all worldwide would-be bookkeepers, requiring them to solve a time-consuming computational “game-of-chance” problem in order to win the honor of entering the next block to the blockchain and the reward of “mining” newly issued Bitcoins, in addition to gaining the transaction fees for all of the transactions included in their block. The Bitcoin network adjusts the degree of difficulty of the problem, in light of the worldwide computational power devoted to solving it, so that it takes just about 10 minutes on average to find a solution.

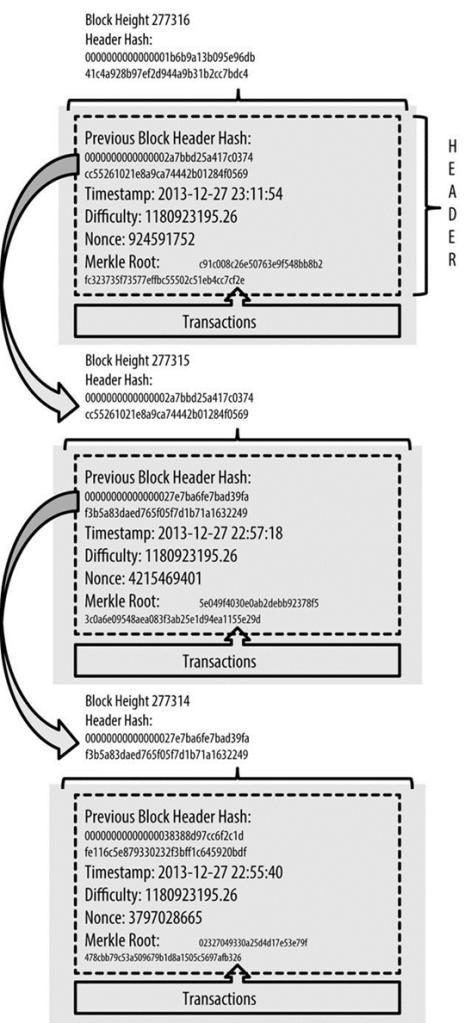

The computational problem to be solved is the generation of a suitable block header cryptographic hash. This can be illustrated with the aid of Fig. II.5, which shows three successive blocks added to the Bitcoin blockchain in December 2013. Each block has a so-called Merkle root (named after one of the developers of hash algorithms), which is a hash generated by SHA-256 from an input string that combines the hash identifiers for every transaction included in the block. The miner’s task is to combine the header hash of the preceding block with the Merkle root for the transactions to be included in the block under construction and with the time stamp for the new block, and then to add at the end of that long string a random integer called a nonce (a number used just once). The latter nonce is then to be varied until the hash created by the new input string contains at least as many zeroes at the start as the Bitcoin network demands for new blocks at the time. Since there is no way other than trial and error to predict the output hash for a given input string, mining competitors simply have to vary the nonce and generate hashes for each nonce value until they produce a winner.

Figure II.5. Three consecutive blocks added to the Bitcoin blockchain in December 2013, indicating for each the header hash of the preceding block, the Merkle root generated from the transactions in the new block, the time stamp, and the random number nonce that generated an acceptable new block header hash beginning with 15 consecutive hexadecimal zeroes.

In the example shown in Fig. II.5, each block header hash began with 15 consecutive hexadecimal zeroes, equivalent to 60 zero bits. The fraction of all possible 256-bit numbers that begin with 60 zeroes is less than 10-18, so it might take as many as a billion billion tries at that random number nonce to generate a new hash differing from the preceding one, but with as many consecutive zeroes at the start. As of April 2022, when more starting zeroes were demanded, the average number of nonce attempts to generate an acceptable header hash is now 122 thousand billion billion! It is very demanding of computer resources to generate a winning nonce; however, once that nonce is revealed to other system nodes, they can very quickly verify the accuracy of the winning block submission and agree to add it to the blockchain. By investing the necessary computational power and providing their winning nonce value to all other nodes, the chosen bookkeeper for the new block provides the “proof-of-work” demanded by the Bitcoin protocol.

Now, the process of assembling and hashing a block is computationally very expensive. It requires massive amounts of machine time, and hence electric power. This is by design. If assembling a block was fast and easy, then a recipe for success would be for an individual or group to create hundreds or even thousands of block creators, and have them submit very large numbers of blocks. But since the creation of blocks is so energy-intensive, it does not make economic sense for individual groups to create large numbers of block creators. The transaction fees are not set by the Bitcoin system, but by the individual who makes a transaction. Block creators tend to include those transactions that offer the highest fees; so the fees will be determined by the amount that users are willing to offer the block creators. In addition to the transaction fees that block creators receive, a creator of a successful block also receives a reward in Bitcoin for successfully adding a block to the blockchain. Therefore, new Bitcoin is created every time a new block is added to the blockchain.

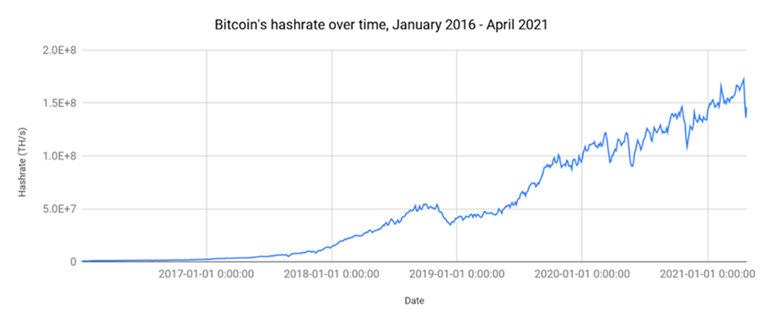

Since the creation and submission of blocks for the blockchain is so labor-intensive, nowadays people who assemble and submit blocks use special computer chips that are called application-specific integrated circuits (or ASICs). These are designed to optimize the process of data mining, and every cryptocurrency has a uniquely created ASIC chip. Thus, there are ASICs designed specifically for Bitcoins, with the goal of increasing the rate at which computers can calculate trillions of cryptographic hashes with SHA-256. A rate of 1 trillion hashes per second is denoted as 1 TeraHash, or 1 TH. As ASIC and computer algorithm designs have improved and the competition within the several billion dollar per year worldwide Bitcoin mining industry has grown fiercer, the cumulative worldwide terahash rate has increased steadily as shown in Fig. II.6, reaching 180 million TH by the beginning of 2022.

Figure II.6. The steady growth over time in the cumulative worldwide terahash rate devoted to Bitcoin mining, reaching 180 million TH by the start of 2022.

With respect to Bitcoin, various countries have sponsored groups of computer experts who have produced and submitted blocks to the Bitcoin blockchain. Figure II.7 shows the percentage of the total computing power in various countries used by computers for Bitcoin mining, as a function of time. In early 2019, China, Russia and the U.S. had the most computer power devoted to Bitcoin mining, with China devoting the vast majority with 75.5%, Russia second with 5.9% and the U.S. third with 4.1%. However, in late 2019, China ceased allowing their computer scientists to participate in Bitcoin mining; in addition, the government has strongly discouraged their citizens from participating in cryptocurrency exchanges. China cited environmental concerns in their decision to ban crypto mining. But, as Chainalysis points out, there may be other motivations as well: “China has a several-year head start in developing Central Bank Digital Currencies (CBDCs), so it may perceive decentralized cryptocurrencies like Bitcoin as competitive with their own centralized alternative.” So, by August 2021, the U.S. was utilizing the largest fraction of time for Bitcoin mining with 35.4%; Kazakhstan was now second with 18.1%, and Russia third at 11.2%.

Figure II.7: The share of total computing power used by computers for Bitcoin mining, by country, as a function of time. In 2019, China had by far the largest share at 75.5%, while Russia was second with 5.9% and the U.S. third with 4.1%. After the Chinese banned Bitcoin mining operations in summer 2019, by August 2021 the largest Bitcoin mining efforts were the U.S. at 35.4%, Kazakhstan at 18.1%, and Russia at 11.2%.

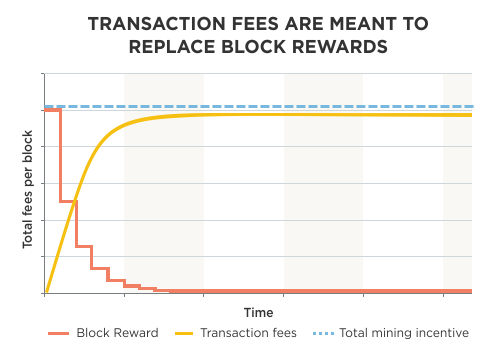

In the Bitcoin system outlined in the whitepaper by Satoshi Nakamoto, the total number of Bitcoins ever produced would be capped at 21 million Bitcoins. In order to accomplish this, the reward for adding a block to the blockchain is designed to decrease in steps as the number of Bitcoins approaches 21 million. Figure II.8 shows the theoretical relation between transaction fees and block creation rewards. As the total number of Bitcoin approaches 21 million, the block reward fees (in newly created Bitcoin) are designed to approach zero. This is shown by the red curve in Figure II.8. Conversely, the transaction fee given to block creators (the yellow curve in Fig. II.8) should increase, in order to make the total fees for block creation constant.

Figure II.8: The theoretical relationship between transaction fees and block creation rewards, as a function of time. Since the total number of Bitcoin is designed to be capped at 21 million, as the number of Bitcoin approaches the maximum, the block reward fees in new Bitcoin are designed to decrease toward zero in regular steps (red curve). The transaction fees (yellow curve) should correspondingly increase, so that the total reward for creating a new block on the blockchain should remain roughly constant.

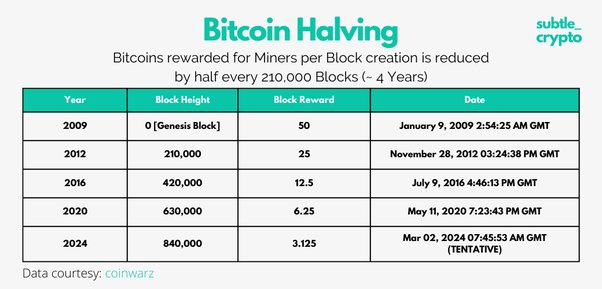

At present (Feb. 2023), about 19.3 million Bitcoin have been created. The mining reward for block creators is designed to halve every time another 1% of the total number of Bitcoin are created (210,000 Bitcoin). The last ‘Bitcoin halving’ took place on May 11, 2020, so that the current reward for creating a block on the Bitcoin blockchain is 6.25 Bitcoin per block accepted, reduced in three steps from the 50 Bitcoin reward at Bitcoin’s 2009 launch. At the current Bitcoin valuation, the reward is equivalent to about US$125,000 to be awarded roughly every 10 minutes. The Bitcoin halvings are shown in Figure II.9. At current rates the next Bitcoin halving is scheduled to occur sometime in 2024. After a halving occurs, the number of new Bitcoin being mined will decrease. In theory, the demand will remain constant, so that after a halving the price of a Bitcoin should increase. However, there is another factor that will determine the value of Bitcoin, namely as the block reward for mining Bitcoin decreases, presumably the incentive for traders to pay increasing transaction fees and for miners to assemble blocks could also decrease. In that case, it might destabilize the Bitcoin system and could drive the value of Bitcoin down. This concern grows more and more important as one approaches the year 2040, when essentially all Bitcoin will already have been generated, the block reward will approach zero, and the entire fee that a block creator is paid will come from transaction fees paid by originators of blockchain transactions.

Figure II.9: The initial block in the Bitcoin blockchain was created on Jan. 9, 2009, and this provided its creator with a reward of 50 Bitcoin. Every time another 210,000 blocks are added to the Bitcoin blockchain, the reward to the creator of the block is halved. The figure shows the date of each ‘Bitcoin halving,’ and the reward for block creation.

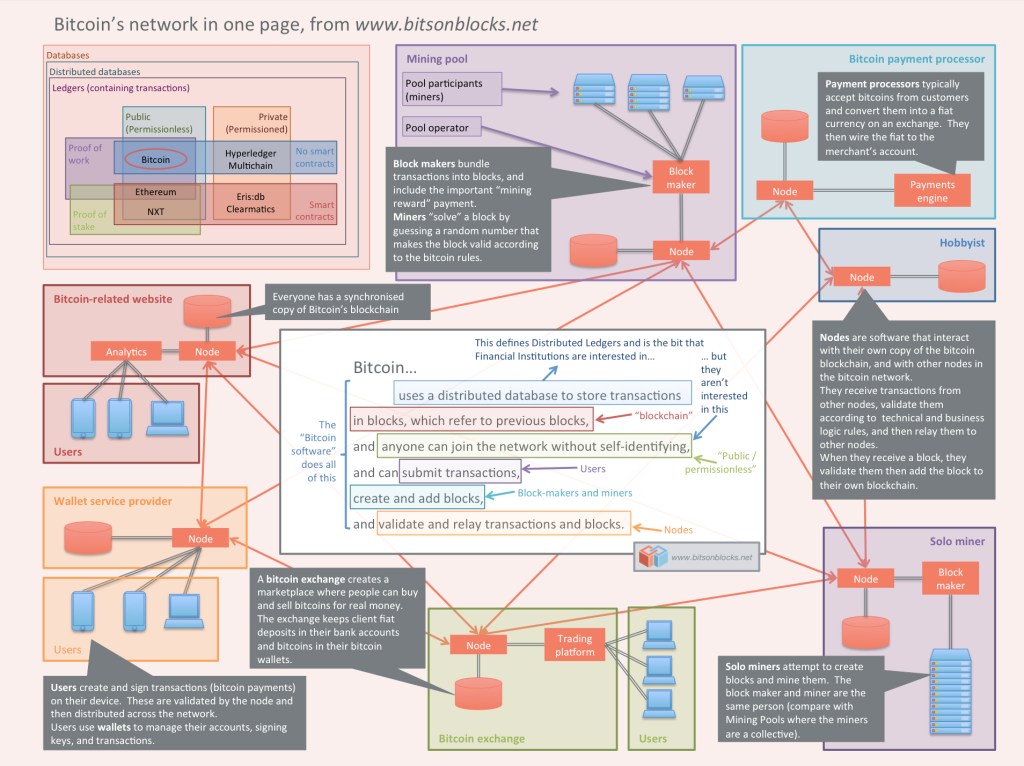

Figure II.10 shows, on a single page, a summary of all of the functions carried out by the Bitcoin blockchain system. Individual users create and sign transactions; those transactions are bundled into blocks by block makers (miners); miners submit blocks to nodes that validate the blocks and add them to the Bitcoin blockchain. A Bitcoin exchange allows individuals to convert Bitcoin into fiat cash and vice versa, using payment processors.

Figure II.10: A Bitcoin Network Infographic. This single page summarizes all of the functions that are carried out on the Bitcoin blockchain network.

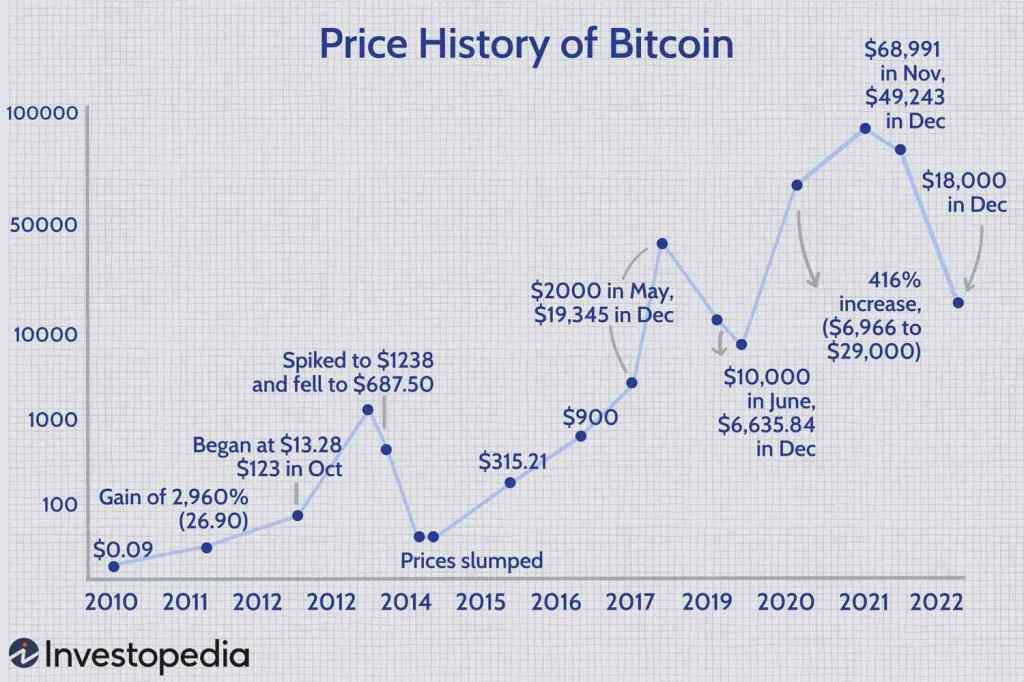

The mechanized system for creating Bitcoin makes it radically different from currency systems such as dollars or Euros. The U.S. Federal Reserve, for example, can influence the number of dollars in circulation by purchasing securities from banks, which encourages lending; or the Fed could sell securities and thus remove dollars from circulation. Bitcoin, on the other hand, is strictly limited in the number that will ever be created. This design feature makes Bitcoin scarce, and the scarcity presumably has contributed to the overall increases in the value of Bitcoin, although that increase has featured a number of volatile rises and falls illustrated in Fig. II.11, including the latest radical drop in value in 2022.

Figure II.11. A coarse history of the price of Bitcoin over time. Note that the price scale in US dollars is logarithmic, so that the sharp rises and falls are quite dramatic.

Another issue is the cost of security on the Bitcoin market. What is the optimal amount that the Bitcoin system needs to pay in order to guarantee protection of their system against hackers? At the present time, the Bitcoin network pays roughly $5 billion per year to guard against thefts and hacks. This has protected the system against attacks by hackers; however, it has not provided security for businesses that are the subject of ransomware attacks. The only quantitative method for determining the optimal cost for network security would be for the Bitcoin system to decrease their payments for security until they began experiencing system-wide hacking; Bitcoin administrators are unlikely to adopt this pragmatic strategy.

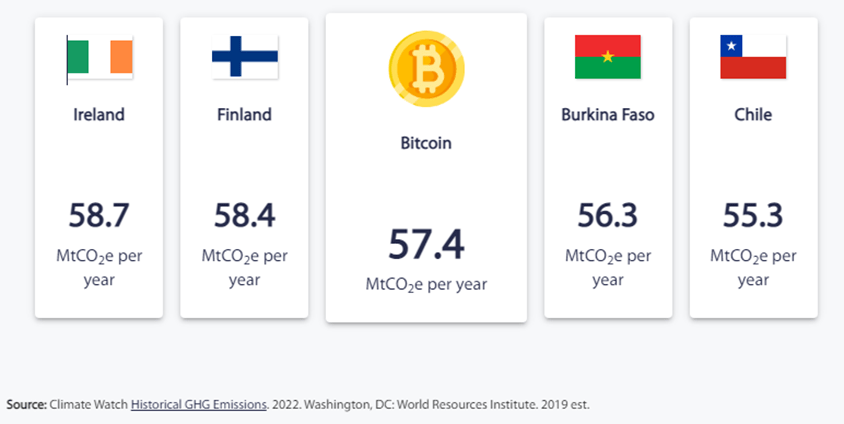

And finally, the cumulative energy consumption of the Bitcoin network, mostly in mining, has become a major consideration in controlling climate change. As of 2022, the Cambridge Centre for Alternative Finance estimates that the worldwide Bitcoin network is consuming about 131 terawatt-hours of energy per year, comparable to the energy use by the entire country of Argentina or Sweden, and accounting for about 0.6% of the world’s total electricity consumption. But the Cambridge group also points out that this usage rate is comparable to the electricity usage in a year by always-on but inactive home devices in the U.S. Both of those constitute unnecessary drains on our worldwide energy resources. The estimated greenhouse gas emissions from worldwide Bitcoin mining in 2019 are compared to those of several other entire countries in Fig. II.12, from the Cambridge Bitcoin Electricity Consumption Index.

Figure II.12. A comparison of 2019 greenhouse gas emissions, in carbon-dioxide-equivalent megatons, estimated for worldwide Bitcoin mining operations and for four entire countries.

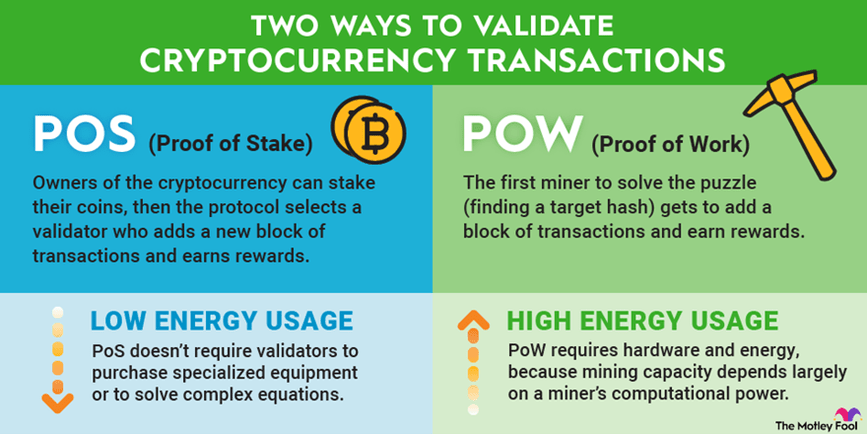

In the case of cryptocurrency, alternatives to Bitcoin such as Ethereum have by now replaced the costly “proof-of-work” protocol with a “proof-of-stake” protocol that requires potential miners to put some of their own currency into a competition for the right to add blocks to the blockchain, thereby avoiding the excessive need for computational power. Proof-of-work and proof-of-stake approaches are contrasted in Fig. II.13.

Figure II.13. A comparison of proof-of-stake and proof-of-work protocols for adding blocks to cryptocurrency blockchains.

Section III: The Ethereum Cryptocurrency:

Ethereum is another form of cryptocurrency. As of this writing (Feb. 2023), Ethereum is the second most popular cryptocurrency, with about half the worldwide market capitalization as Bitcoin, but higher transaction volume. The coin associated with Ethereum is Ether (ETH). Ethereum was created in 2013 by Vitalik Buterin, with assistance from a number of associates. Ethereum went public on July 30, 2015. Like Bitcoin, Ethereum provides a way for transactions to take place without relying on any third-party companies or individuals such as banks and bankers. Ethereum shares a number of features with Bitcoin. First, Ethereum relies on a network of public keys and private keys that enable pseudonymity of users and transactions by means of cryptography. Ethereum also maintains a blockchain, which contains a permanent record of all transactions on that network.

While the Bitcoin blockchain is updated by adding a new block to the blockchain every 10 minutes, the Ethereum blockchain is updated every 12 seconds, allowing for faster transaction processing. Each new block contains a cryptographic hash, which lists all preceding blocks on the blockchain. This enables observers to track the chronological progression of the blockchain. The Bitcoin blockchain incentivizes bookkeepers who load blocks with transaction fees that are offered by individuals in return for adding their transactions to a given block. On the Ethereum blockchain, the function of transaction fees is accounted for by gas. Gas is the amount of ETH that the sender of a transaction must pay to the network, in order that the transaction can be included in the blockchain. Transactions in Ethereum are executed through the Ethereum Virtual Machine or EVM. The EVM consists of a set of instructions, memories and storage for all Ethereum accounts. EVMs have been implemented in a number of different programming languages, including C++, Java, Javascript, Python and Ruby. The EVM guarantees that a given transaction will produce the same post-transaction state for any of the programming languages in which it is implemented.

Each different operation that can be performed by the EVM comes with its own gas cost, which is intended to be proportional to the value of the computer resources that are required to compute and store the result of that operation. The person submitting a transaction specifies a gas limit (the maximum amount of gas the person is willing to pay for the transaction), and a gas price (the amount of ETH the person is willing to pay, per unit of gas used). The transaction will only be added to the block if the gas price offered is greater than or equal to a base gas price for that transaction. When the gas price is greater than the base gas price, the excess represents a tip that is offered as an incentive for the block proposer to add the transaction to their block. The greater the tip, the faster the transaction will be included in a proposed block.

Ethereum was designed to include a number of functions that were not allowed in the Bitcoin system. All Bitcoin are identical; therefore they can be interchanged and thus are fungible (i.e., capable of substitution or interchangeable). In addition to ETH tokens, the Ethereum system also allows transactions involving unique tokens that are tied to a particular object and are not interchangeable, thus they are non-fungible tokens or NFTs. For example, people playing online games may be offered an NFT denoting that they have purchased or earned a sword, or magic wand, or other asset. Alternatively, a person may purchase an NFT that provides them with a digital representation of a painting or sculpture. The most expensive NFT as yet created was produced by the artist Beeple. It was titled Everydays: the First 5000 Days. It is a collage made up of 5,000 separate NFTs, and it is reported to have taken 13 years (approximately 5,000 days) to create. In March 2021, the Everydays collage was sold at a public auction at Christie’s for $69, 346,250.

Figure III.1: Detail from the collage Everydays: the First 5,000 Days by Beeple. This is a collage made from 5,000 separate digital NFTs. In March 2021 it was sold by auction at Christie’s for over $69 million dollars US.

One of the goals of the Ethereum system was to allow applications for not only money, but also for assets such as stocks or property. The Ethereum system was developed to include aspects of decentralized finance or DeFi, such as “a broad array of financial services without the need for typical financial intermediaries like brokerages, exchanges, or banks, such as allowing cryptocurrency users to borrow against their holdings or lend them out for interest.” This was accomplished through the development of smart contracts in a 2018 yellowpaper by Gavin Wood. In cryptocurrency systems such as Ethereum, a smart contract is a computer code that is activated on a blockchain or other distributed ledger. Some smart contracts are used to produce legally binding agreements executed on the blockchain; these are called smart legal contracts. However, more generally a smart contract could be any computer program that executes an action on the blockchain. That action is validated by a digital signature authenticated by the participants; it is stored on the blockchain and cannot be changed.

The adoption of smart contracts allows the Ethereum network to be capable of more types of transactions than Bitcoin. As a result, the Ethereum network has become a popular site for transactions involving NFTs. Also, initial coin offerings for other cryptocurrencies are often initiated on the Ethereum network. Smart contracts are also a central feature in the thriving DeFi sector, where peer-to-peer financial transactions eliminate the fees that banks and other financial companies normally charge for serving as intermediaries in such transactions. Transaction volume in the DeFi sector has grown especially rapidly since 2020.

A major success of the Ethereum blockchain was the creation in March 2017 of the non-profit Enterprise Ethereum Alliance (EEA), which had 30 founding members. By May 2017 the EEA had 116 members including Samsung, Microsoft, Intel, J.P. Morgan, Deloitte, Accenture, and the National Bank of Canada; and by July 2017 the alliance had 150 members including groups like MasterCard and Cisco Systems. Figure III.2 shows some of the members of the EEA Alliance.

Figure III.2: Corporate logos of some of the members of the Enterprise Ethereum Alliance or EEA, as of May 2017.

One of the big advantages of DeFi was that the computer code for smart contracts Is publicly available to everyone on the Web. Thus, any user can view the language in a smart contract. Unfortunately, it turns out that a number of smart contracts have vulnerabilities in their computer code. Hackers can exploit these vulnerabilities and can divert resources from users to their own accounts. According to Investopedia, because DeFi has been largely unregulated, “its ecosystem is riddled with infrastructural mishaps, hacks, and scams.” As we mention in Section V, in the past couple of years billions of dollars have been stolen from participants in DeFi transactions.

In addition to this type of theft, Ethereum networks have also been plagued by thefts from computer hackers. A decentralized autonomous organization or DAO was developed around a set of smart contracts that were designed to allow a DeFi system to be created on the Ethereum platform. But in 2016 a hacker stole $50 million worth of DAO tokens. As a result of this theft, the Ethereum system “forked” into two different blockchains. The Ethereum Classic blockchain continued, with the loss of $50 million in tokens. A new blockchain, now called Ethereum, forked off from the original blockchain; in Ethereum the blockchain began with the theft being reversed.

Initially, the Ethereum system used the same “proof-of-work” (PoW) system to add blocks to the blockchain as was employed by the Bitcoin network. However, as pointed out above, the PoW method uses incredible amounts of computer time to implement. The energy costs associated with PoW are so severe that in Sept. 2019 China’s National Development and Reform Commission declared that Bitcoin mining was an “undesirable” action that should be restricted or phased out by local governments. Shortly afterward, Bitcoin mining was removed from this list of undesirable actions; however, in May 2021, the Chinese State Council called for restrictions on both mining and trading of cryptocurrencies. Before 2019, China had been the predominant world power engaged in Bitcoin mining; however, at present Bitcoin mining in China has essentially disappeared, as was shown in Fig. II.7.

In Sept. 2022, Ethereum changed from “proof-of-work” to a system called “proof-of-stake” or PoS (see Fig. II.13), which had been first adopted by another cryptocurrency called Cardano. While the Bitcoin system incentivizes miners to load blocks onto the blockchain, in the Ethereum system these are called validators. In the PoS system, validators are people who possess large quantities of the crypto token (for Ethereum this is ETH). The rationale is that people with large amounts of Ether will not participate in actions that will harm the blockchain system; conversely, in order to mount an attack on the blockchain, attackers would have to acquire very large amounts of the currency token to become validators. A user’s coins are locked from availability while they stake them in hopes of validating new blocks. As explained by the Motley Fool, “Participants who stake more coins are more likely to be chosen to add new blocks…There’s usually an element of randomization involved, and the selection process can also depend on other factors such as how long validators have been staking their coins.” A major reason for switching from the PoW system to PoS is that the proof-of-stake system does away with the requirement that block formation takes enormous amounts of computer time. Ethereum administrators estimate that the switch to a PoS system has reduced the computational time and energy necessary to load a block by 99%.

Unfortunately, the advantage of the PoS method, namely that it greatly reduces the computer time necessary to create and load a block onto the blockchain, also comes with its own disadvantages. Because the PoW blockchain requires enormous amounts of computer time to load a block, it is nearly impossible to alter earlier blocks in the chain; the computing time required to do this is daunting. However, since the PoS method requires so little computational time to create and load a block, this also makes it relatively easy to modify earlier blocks on the blockchain. This has led to two different types of attacks on the PoS blockchain. The first is called a long-range attack. In such an attack, a significant portion of the main blockchain is replaced with a ‘hijacked’ version. A second attack, called a short-range attack, replaces only a small portion at the end of the chain.

If hackers succeed in removing earlier validated blocks and replacing them with their own blocks, then in theory it would be possible to double-spend, or to spend the same cryptocurrency on two different transactions. The solution to this is either to penalize validators who accept conflicting chains, or to remove the incentive to approve conflicting chains. Many groups who use PoS methods have adopted a system called Byzantine Fault Tolerance, which is believed to prevent the validation of conflicting chains.

Unlike Bitcoin, Ether is not designed to be a finite resource with a cap on the total number of coins in circulation. This accounts for some differences in the way the two cryptocurrencies are typically used and also in their valuation. For example, Chainalysis data from July 2021 reveals that 73% of Bitcoin is held by long-term investors, whose crypto wallets still contain at least 75% of all the cryptocurrency they’ve ever received. The corresponding fraction of long-term investors for Ethereum is 58%, and it is worth noting that Ethereum has been around six fewer years than Bitcoin. Bitcoin is held in user wallets for an average duration of about 3 years, while Ether is held for an average of 1.5 years.

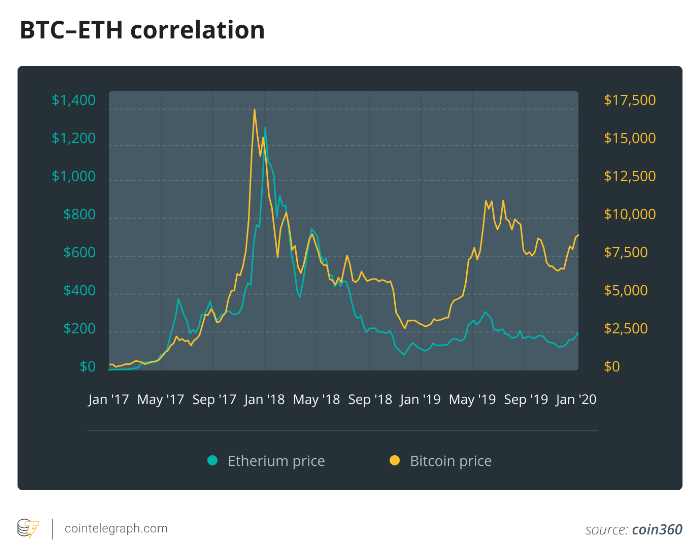

While Ether does not share the ultimate scarcity aspect of Bitcoin, its price valuation is, like that of Bitcoin, driven by supply and demand, in analogy to the prices of traded stocks. As Fig. III.3 makes clear, there is some degree of correlation between Bitcoin and Ether prices, although the latter tend to run more than a factor of ten below the Bitcoin price. When demand is high for Bitcoin, it tends to increase as well for Ethereum. When prominent scams and exchange collapses in the crypto sector occur, they tend to induce nervousness and produce selloffs for all cryptocurrencies. However, as DeFi transactions become more popular, one may expect Ether to gain some ground on Bitcoin.

Figure III.3. The price valuations of Bitcoin (yellow curve, right-hand scale) and Ethereum (blue curve, left-hand scale) from 2017 through 2019.

In the wake of the success and growing market value of Bitcoin and Ethereum, there have been any number of competitor digital currencies. Some of these are mere copycats, occasionally with the aim of scamming purchasers out of their funds, while other have added innovative features to the use of blockchains. The Motley Fool points out that, as of the end of June 2022, more than 12,000 distinct cryptocurrencies had been introduced, with the number more than doubling from 2021 to 2022. They provide the table below to highlight differences among the most successful, ongoing cryptocurrencies.

| CRYPTOCURRENCY | DESCRIPTION |

| Bitcoin (CRYPTO:BTC) | The first cryptocurrency and the largest by market cap. |

| Ethereum (CRYPTO:ETH) | The cryptocurrency with the first programmable blockchain that developers can use to build decentralized apps (dApps). |

| Tether (CRYPTO:USDT) | A stablecoin that follows the U.S. dollar and the cryptocurrency with the most trading volume. |

| Cardano (CRYPTO:ADA) | A research-based cryptocurrency that’s more environmentally friendly due to its low energy usage. |

| Binance Coin (CRYPTO:BNB) | The native cryptocurrency on the Binance Smart Chain, which was built by the popular Binance exchange. |

| XRP (CRYPTO:XRP) | The native cryptocurrency for Ripple and the subject of an SEC lawsuit alleging that it’s an unregistered security. |

| Polkadot (CRYPTO:DOT) | A cryptocurrency designed to allow different blockchains to communicate and work with each other. |

| Solana (CRYPTO:SOL) | A cryptocurrency with a high-performance blockchain capable of ultra-fast and inexpensive transaction processing. |

| Dogecoin (CRYPTO:DOGE) | The first memecoin to gain widespread popularity. |

| Monero (CRYPTO:XMR) | A donation-based cryptocurrency that intends to provide total privacy through untraceable transactions. |

— To Be Continued in Part II —