Addendum Feb. 20, 2024: A reader of our post, Jeffery Breed, sent us a message to alert us to a Crypto investment fraud network. An article by cybersecurity researcher Jeremiah Fowler explained how he was alerted to a cryptocurrency investment fraud when a friend contacted him to ask how they could recover their money from a firm. The scam worked as follows. A person is contacted by a group claiming to be a legitimate investment firm. They are offered an opportunity to invest in a product that is guaranteed to produce amazing returns. The victims are contacted by various methods – cold calls, Websites that appear to be reputable, or contacts through social media that claim to be from friends or acquaintances of the victim. Although the sites claim to accept many forms of payment such as major credit cards, when the victim attempts to make a deposit, the firm will only accept payment in Bitcoin.

The victims are also told that prices of their commodities are rising so rapidly that investments must be made immediately. Initially, this appears to be a legitimate investment; the victim may be able to make withdrawals for a short while, or they are told that large amounts of profit have been deposited into their account. They are then informed of the opportunity to invest more funds into “preferred” accounts that may promise returns as large as 20% per month. However, at some point when the victim attempts to withdraw funds, they are told that in order to withdraw the funds “smoothly,” they must “upgrade” by paying an additional sum. The demands for additional funds continue until eventually the victims realize they are never going to get their money back.

When Jeremiah Fowler investigated further, he found that the perpetrators of this scam had registered nearly 300 different Websites on more than a dozen different domain hosts. Frequently, the scammer opens a Bitcoin “wallet” for each victim; as soon as the victim has deposited a sufficient amount of funds, the money is withdrawn and the wallet is closed. This makes it extremely difficult for the transactions to be traced back to the perpetrator. Although Fowler reported the scams to the Web hosts and the police, he received very little cooperation from either group. The police were often unable to help as the scammers were located in remote countries. Web hosting providers often required that the victim had to contact them directly, and victims were required to provide proof that they had contacted the police.

Web hosting services could cut down on these scams by requiring anonymous site registrations to provide systems that are used by banks and credit institutions to identify their customers. In that case, the hosting services would be able to identify the perpetrators when crimes occur. States or the federal government could require Web hosts and domain registrars to securely identify their clients. In the meantime, individuals need to do their own due diligence. They need to avoid unsolicited offers, to be skeptical of offers that seem “too good to be true,” and to thoroughly research sites where they will invest their money. Individuals also need to resist pressure to make investments immediately, and to rely on advice from trusted financial advisors.

As we show in our posts on cryptocurrency, at present these markets are operating in a “Wild West” environment where regulations are sparse, scams proliferate, and many cryptocurrencies operate in an atmosphere of extreme volatility. We urge authorities to regulate this industry, in order to minimize the ability of bad actors to prey on gullible investors.

Jeremiah Fowler, How

I Accidentally Uncovered a Crypto Mining and Investment Fraud Network,

vpnMentor, Aug 7, 2023

March 1, 2023

Section V: Are Cryptocurrencies Fulfilling Their Promise?

The goal of cryptocurrency was to provide a financial system that could successfully compete with the current world of financial institutions, and that could thrive as a system that would function in the absence of banks or other financial institutions, and in the absence of government currency minting operations, by utilizing cryptographic techniques. In this section we will review the extent to which Bitcoin and Ethereum now constitute a viable alternative to banks and other financial institutions.

A first requirement for a successful financial institution is that it be stable. We can first analyze the stability of crypto by examining the fluctuations in value of cryptocurrency vs. time. Figure V.1 shows the value in US dollars of Bitcoin, as a function of time. The graph shows a dizzying sequence of peaks and valleys, driven by dramatic changes in supply and demand for Bitcoins. The value of a single Bitcoin was $77 in July 2013. However, in mid-2017 Bitcoin rose sharply to around $20,000 and then lost half its value in a short period of time. Beginning in mid-2018, the value of Bitcoin increased rapidly to about $60,000; however, it quickly lost half its value. Bitcoin again increased rapidly in value, and in Nov. 2021 it peaked at over $67,000 for one Bitcoin. However, this was followed by a rapid drop in value to roughly $20,000 in the first half of 2022.

Figure V.1: The value of one Bitcoin as a function of time from 2013 through the first half of 2022. In July 2013, one Bitcoin was worth $77 dollars. In Nov. 2021 the value of Bitcoin peaked at over $67,000. By mid-2022 it had decreased to about $20,000.

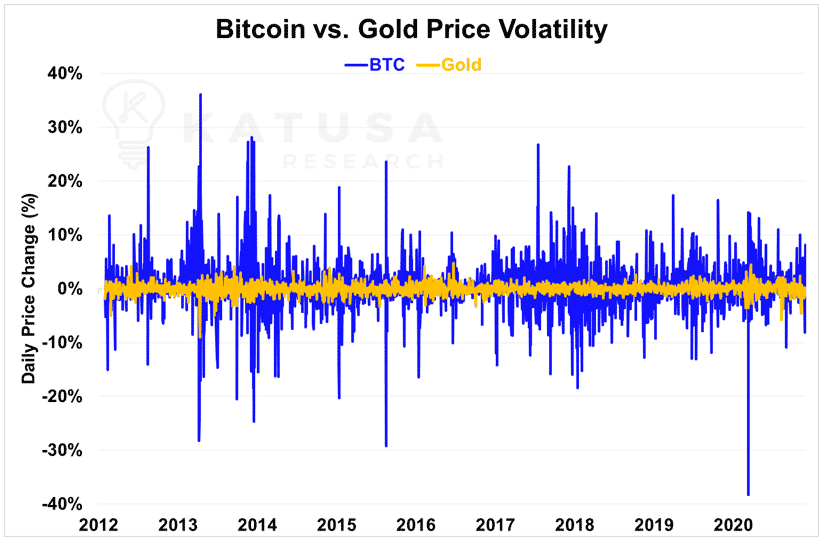

Over the past few years, Bitcoin values have seen very sharp fluctuations. The value of Bitcoin is therefore highly volatile; in fact, the rapidly fluctuating value of Bitcoin is nothing like the stability desired for a viable financial product. It is more akin to a very high-risk stock. In Figure V.2 we show the volatility of Bitcoin over time, compared with the volatility of another alternative currency, gold. Over the period 2012 to 2021, the daily value of gold almost never fluctuates by more than one or two percent. On the other hand, daily price changes in Bitcoin exceed 20% (up or down) on several occasions during this time period.

Figure V.2: The volatility of Bitcoin (blue curve), the daily percent changes in price of Bitcoin, vs. the volatility of gold (yellow curve), from 2012 to 2021. During this period, the volatility of gold almost never exceeds one or two percent changes. By contrast, there are several occasions during this period when the volatility of Bitcoin exceeds 10 percent.

The high volatility of Bitcoin and other cryptocurrencies suggests that a major reason for holding such assets may be for speculative purposes, to wager on (or for big investors, such as Tesla, to drive) rapid upward or downward excursions in value. In Dec. 2021, Aristides Capital Manager Chris Brown commented that Fed interest rate hikes might negatively impact cryptocurrency markets. He pointed out that a major feature of cryptocurrency is its purchase by speculators. Brown noted that “The prime example of such asset speculation is cryptocurrency; here lies $2.64 trillion of ‘wealth’ that is backed by nothing and generates no cash flows.”

So, the rapidly fluctuating value of Bitcoin and other cryptocurrencies is a strong negative incentive to view these as stable currency systems. Indeed, their volatility has led to the growing popularity of so-called stablecoins, which are digital currencies whose value is pinned in principle to a more stable asset, such as the US dollar or the price of precious metals. To date, however, stablecoin issuers have yet to prove that they maintain sufficient reserves to support that promised stability.

Even more concerning than the volatility is the number of cryptocurrency companies that have failed. The Website 99Bitcoins.com lists over 1,700 cryptocurrencies or cryptocurrency exchanges that have failed, as of Jan. 2023. This is an astonishing rate of failure and suggests that the field of cryptocurrency is still a “Wild West” arena, with companies starting up and failing with incredible frequency.

Even worse, the reason behind the failure of these companies is also exceedingly opaque. As reported by CoinJournal, only 22% of cryptocurrency exchanges that closed down failed because of “normal business reasons.” Another 5% of the exchanges shut down after being hacked and having their resources stolen, 9% of the exchanges turned out to be scams, and 8% of the exchanges closed under pressure from regulators. But an astonishing fraction, 42%, of these exchanges “just disappeared;” that is, they ceased activity and their Websites went down, but without any explanation. The reason for failure of cryptocurrency exchanges is shown in Figure V.3.

Figure V.3: The reasons for failure of cryptocurrency exchanges, from CoinJournal.com. Of the exchanges that closed down, only 22% failed for “normal business reasons.” 5% of the exchanges shut down after a hacking attack, 9% were simply financial scams, and 8% of the exchanges were shut down for regulatory reasons. 42% of these exchanges “just disappeared;” they ceased activity and their Websites went down, without any stated reason.

A second feature of a viable alternative currency is that it be secure. We have seen that at present, cryptocurrency is highly insecure. First, because there is no central company such as a bank that holds your crypto assets, your ability to access your assets relies totally on your private key password. These keys are not easily memorized; both Bitcoin and Ethereum use 256-bit, or 64 hexadecimal character, strings or equivalent QR codes for private keys. If you lose your password, there is no way you can access those funds – there is no such thing as a “forgot your password?” prompt. At the moment, nearly 4 million of an eventual maximum 21 million Bitcoins issued appear to be in wallets to which their owners have lost access. Also, if someone is able to discover your private key password, they can gain access to all of your crypto assets and transfer them to their own accounts. Since the private key password consists of a long string of random letters and numbers, people need to create lists of all their crypto passwords and store them in a secure location. Many people create a computer folder and store their passwords there. This has led to opportunities for hackers. They search people’s computer files for private key passwords; they copy the passwords and use them to access crypto assets.

Although some hackers target individual crypto accounts, a more lucrative practice for hackers is to try to break into cryptocurrency exchanges and extract their funds. From Fig. V.3, we see that 5% of closed exchanges failed because their assets were hacked. There is no equivalent of the Federal Deposit Insurance Corporation to ensure your crypto savings against exchange failures if you store one or more wallets on those exchanges. One of the first crypto exchanges to be hacked was the Mt. Gox exchange in 2014. Here we will briefly review the history of the Mt. Gox exchange.

The Mt. Gox Exchange and its Demise:

In 2006, Jeb McCaleb was motivated to build a website that would allow online gamers who played Magic: The Gathering to trade cards from that game, much like people trade stocks. McCaleb created the domain name mtgox.com, which stood for “Magic: The Gathering Online EXchange.” McCaleb subsequently became interested in cryptocurrency, and he used the mtgox.com Website to create an exchange that would allow people to trade cryptocurrency, and to move funds between dollars and crypto.

In March 2011, McCaleb sold the mtgox.com site to a French developer, Mark Karpeles. Mtgox.com then became a highly successful cryptocurrency exchange site. By early 2014, it was handling over 70% of all worldwide business in the Bitcoin cryptocurrency BTC. At the same time, Mt. Gox experienced a series of irregularities in its business. On several occasions, the exchange reported that large amounts of Bitcoin appeared to be missing. In addition, from time to time depositors would be unable to access their assets. In 2013, the Mt. Gox problems accelerated as the company came under pressure from the U.S. Immigration and Customs Enforcement, which claimed that Mt. Gox was operating as “an unregistered money transmitter in the U.S.” In Nov. 2013, Wired magazine reported that Mt. Gox customers were experiencing long delays in accessing their funds; the article stated that Mt. Gox “had effectively been frozen out of the U.S. banking system because of their regulatory problems.”

The coup de grace for Mt. Gox began on Feb. 7, 2014, when the company halted all Bitcoin withdrawals, stating that they had discovered bugs in the Bitcoin software, and that they would resume normal transactions once those bugs were corrected. On Feb. 24, Mt. Gox suspended all trading and its Website went blank. Someone accessed an internal company crisis management document stating that Mt. Gox was insolvent and that it had lost Bitcoins worth roughly $473 million in a theft that had apparently been going on unreported since 2011; that document was subsequently leaked. The U.S. Dept. of Justice subsequently named Alexander Vinnik, the Russian owner of the BTC-e Bitcoin exchange, as a major figure in extracting and laundering Mt. Gox’s stolen Bitcoins.

In August 2015, Japanese police arrested Alex Karpeles and indicted him on a number of charges related to fraud and embezzlement (the Mt. Gox exchange headquarters was in Japan). There were two major aspects of these charges: the first charge alleged that Karpeles had falsified data to inflate the apparent size of the Mt. Gox BTC holdings; the second charge was that Karpeles had illegally moved the assets of other trading accounts into his own account, some six months before the collapse of that company. Karpeles was convicted of falsely inflating the value of Mt. Gox’s holdings; he was sentenced to 30 months in prison, but that sentence was suspended.

From Fig. V.3, we see that another 9% of failed cryptocurrency exchanges were because they were simply financial scams in which exchange owners extracted users’ holdings for their own enrichment. Various types of cryptocurrency scams continue to be operated and to prey on unsuspecting investors. There is a private sleuth, Danny de Hek of New Zealand, who identifies himself as the “Crypto Ponzi Scheme Avenger.” De Hek searches for cryptocurrency exchanges that promise unbelievable rates of return; he investigates their promises and practices, and then exposes them in YouTube videos. He has gained sufficient fame that his viewers now send him links to suspicious sites that he reviews.

Incidents of hacking continue to occur on cryptocurrency exchanges. However, a related field called decentralized finance or DeFi has recently experienced a new series of major hacks. In the field of DeFi, people are able to lend, borrow and conduct business without relying on banks as central repositories of funds, or lawyers to draw up legal agreements between participants in economic endeavors. The cryptocurrency Ethereum, which uses the crypto coin ETH, has pioneered the use of “smart contracts.” These are agreements codified in computer code within the blockchain that groups can enter into in order to perform various economic functions. Some smart contracts are intended to be legal documents. Other smart contracts enable other decentralized business agreements to be enacted.

One feature of decentralized finance that has been very attractive is that investors are able to take out loans without disclosing their identity; also, credit checks are not carried out before a loan can be processed via DeFi. It is estimated that approximately $100 billion in cryptocurrency has been invested in a host of DeFi projects. Since Ethereum has been the leader in the development of smart contracts, much of this has involved the use of the Ethereum currency ETH. The smart contracts are based on open-source code, so that everyone is able to view the code that enables a smart contract. Unfortunately, some of the smart contracts are based on software code that contains vulnerabilities. Using their ability to view and analyze these contracts, hackers have discovered and exploited these vulnerabilities.

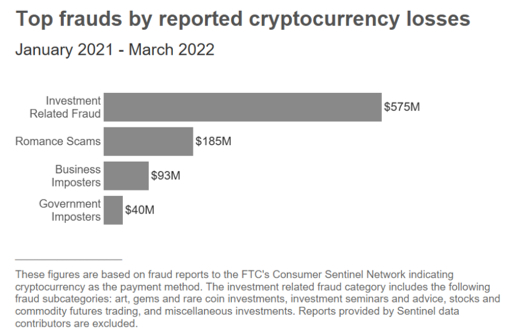

When bad actors are able to hack into the smart contracts, they have access not just to a single user’s assets, but they have been able to mount attacks on the infrastructure of the smart contract. This enables them to divert assets from all accounts that use the smart contracts. The net result has been a terrifying diversion of cryptocurrency assets. The crypto tracking firm Chainalysis estimates that in the past year $2.2 billion has been stolen from decentralized finance projects by hackers. Figure V.4 shows estimates by the Federal Trade Commission of the top frauds relating to cryptocurrency. During the period January 2021 – March 2022, the FTC found that $575 million had been stolen in investment-related fraud.

Figure V.4: The top cryptocurrency frauds as estimated by the Federal Trade Commission, during the period Jan. 2021 – Mar. 2022. During that period the FTC found $575 million stolen in investment-related fraud, $185 million in “romance scams,” $93 million by business imposters and $40 million by imposters claiming to be representing the government.

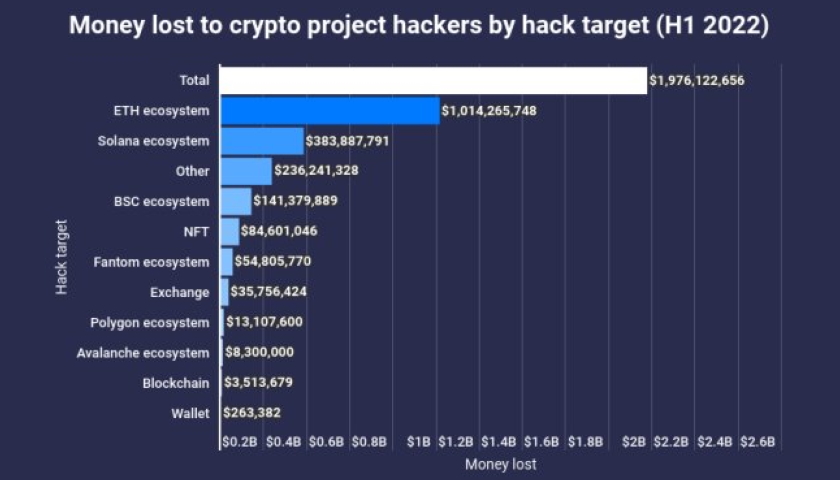

Figure V.5 shows estimates of the cryptocurrency funds that were stolen by hackers during the first half of 2022, broken down into the cryptocurrency exchanges that lost the most money. Nearly $2 billion was stolen, in a total of 175 hacks. The biggest target by far was the Ethereum network. Over $1 billion was stolen on the Ethereum ecosystem alone (note: because the price of crypto varies so dramatically, the value of a given hack is calculated using the conversion rate of that currency at the time of the hack). According to a New York Times article by David Yaffe-Bellamy, notable hacks included $180 million from the software platform Beanstalk, $190 million from the Nomad platform and $160 million from Wintermute. In March 2022, hackers sponsored by the North Korean government stole $620 million in cryptocurrency from the Ronin Network, which runs the video game Axie Infinity.

Figure V.5: Estimates of funds that were stolen by crypto project hackers during the first half of 2022. The total of all stolen funds was $1.976 billion, and is broken down by the exchanges from which the funds were stolen. By far the largest individual loser was the Ethereum ETH ecosystem, which suffered over $1 billion in losses.

A company called Wormhole specialized in what are called cross-chain bridges. A cross-chain bridge allows investors to switch funds back and forth among different blockchains, enabling users to rapidly move their assets from one cryptocurrency to another. Such bridges have become very popular among cryptocurrency users, and the bridges have allowed very large sums to be transferred among cryptocurrency platforms. This has proved an inviting target for hackers. According to the cryptocurrency security company Chainalysis, ten hacks in the past year have involved cross-chain bridges, and $1.3 billion has been stolen in these hacks. In response to these thefts, companies specializing in security for crypto assets have proliferated. Although it is possible that cybersecurity associated with cryptocurrency will eventually close these loopholes, at the present time it must be said that cryptocurrency finance is rife with opportunities for hackers to exploit. The current cryptocurrency situation is the exact opposite of a secure financial ecosystem.

A third requirement for a viable currency system is that it be widely accepted in the financial world. This is yet another instance where cryptocurrency fails the test. After Bitcoin was first unveiled, a few companies began to accept Bitcoin as an acceptable form of currency exchange. However, very few retail establishments now use Bitcoin or other cryptocurrencies in ordinary transactions. Establishment economists, including numerous Nobel Prize winners, have frequently dismissed the long-term utility of cryptocurrency, even while finding potentially useful, more limited, features of blockchain and smart contracts. For example, Joseph Stiglitz has argued that cryptocurrencies should be outlawed; James Heckman has compared the widespread use of crypto to the speculation that drove tulip mania in 17th century Netherlands; Robert Shiller has summed up the opinion of many economists by saying “it’s such a wonderful story. If only it were true.”

Aside from investment purposes, there are a few businesses where cryptocurrencies are widely used. Of course, cryptocurrency has become a popular, if risky, tool for investors, and has established a significant foothold. Another business where cryptocurrency is in wide use is the video and online gaming community. People who use online casino gambling programs are used to dealing in tokens, as casino chips are an early analog of cryptocurrency tokens. Many fantasy video games have merchandise such as cards or other digital assets. Such games can offer tokens that their players can purchase or trade, and in several of these games cryptocurrency can be used as the standard form of payment. Gamers are attracted in part because of the anonymity afforded by crypto, and the fact that they don’t have to use third-party payment processors such as credit cards or PayPal. Cryptocurrency exchanges have also claimed that transaction fees will be significantly less than fees charged by traditional lenders; however, at present crypto transaction fees are generally larger than fees charged by credit cards.

A significant improvement in online gaming is that cryptographic methods can be used to produce provably fair results in gambling. The easiest explanation of provable fairness is with gambling examples that rely on a single outcome, such as the spin of a roulette wheel. If one is playing a video game of roulette, the game will be fair if the outcomes of the roulette wheel spin are random. Until now one has had to trust the operator of the gaming site, or to assume that the site is properly regulated, to assure that the results are being generated in a truly random fashion. Furthermore, one assumes that the outcome of the roulette wheel spin was determined before the gamer placed a bet; otherwise, the game operator could wait until the bet was placed, and then manipulate the roulette wheel result to cheat the bettor.

In a provably fair system, two seeds of random numbers are generated using a cryptographically generated hash. Those seeds are used to generate a final outcome for the spin of the wheel. The bettor is sent an encrypted version of the seeds before she places her bet. After the outcome, the bettor receives the seeds in a non-encrypted format. If the before and after seeds match, the bettor can be assured that the game operator did not cheat them. In addition, the online casino provides the source code for its provably fair games. In theory, the bettors could examine the code to convince themselves that the game is in fact fair.

One final area where cryptocurrency is having a negative impact involves the amount of computer time needed to process and submit a block to the Bitcoin blockchain. Data mining on the Bitcoin system requires the use of computer time (and hence energy) that is so large that it is having a significant impact on the rate of global climate change, as we have already discussed briefly in Part I of this post. In a 2022 article in Nature Scientific Reports, Jones et al. studied the economic impact of data mining for the Bitcoin cryptocurrency. They used three measures for the sustainability of this crypto system, and they reported that the current system of Bitcoin mining fails all three. Jones et al. concluded “We find that for 2016–2021: (i) per coin climate damages from BTC were increasing, rather than decreasing with industry maturation; (ii) during certain time periods, BTC climate damages exceed the price of each coin created; (iii) on average, each $1 in BTC market value created was responsible for $0.35 in global climate damages, which as a share of market value is in the range between beef production and crude oil burned as gasoline, and an order-of-magnitude higher than wind and solar power. Taken together, these results represent a set of sustainability red flags. While proponents have offered BTC as representing ’digital gold,’ from a climate damages perspective it operates more like ’digital crude’.” This analysis makes cryptocurrency systems that rely on proof-of-work “data mining” appear to be seriously unsustainable.

In summary, we have shown that cryptocurrencies fail several requirements for a viable alternative currency. At present, cryptocurrency is remarkably volatile and has yet to demonstrate stability. It is also dangerously insecure, as demonstrated by the number and size of major hacks to crypto exchanges, and the large number of crypto companies that turn out to be scams or Ponzi schemes. These issues are not surprising for a system where your assets are backed by computer records rather than bank vaults, and you generally have no idea with whom you are making deals. Finally, cryptocurrency is not widely accepted for many commercial purposes; for ordinary purchases such as food or clothing, relatively few establishments accept cryptocurrency. Despite all of these issues, cryptocurrency has for now been accepted for use by some 200 million individuals. As illustrated in Fig. V.6, 10% worldwide of internet users between the ages of 16 and 64 own or have owned at least some cryptocurrency. In some countries, that fraction rises to 20%; of course, in some countries the government-backed currency is itself not very robust or subject to high inflation.

Figure V.6. The fraction of internet users between the ages of 16 and 64 who own or have owned at least some cryptocurrency, as a function of country. The worldwide average is 10.2%.

Crypto: What Will the Future Bring?

The current situation is that blockchain technology is widely used for investment purposes, has gained a strong foothold in certain areas such as online gaming, and is also being used to finance a wide variety of illegal material. The original premise that cryptographic techniques make it impossible to track the flow of money through the blockchain has proved to be wrong. With the original public blockchain for the dominant Bitcoin technology, it is now possible to trace the flow of funds. This ability, spearheaded by companies such as Chainalysis, has allowed the U.S. and western governments to take down illegal enterprises such as the Silk Road anonymous marketplace and several of its successors. Teams of agents from various western democracies have also busted the Welcome to Video hub for child sexual abuse materials.

Nevertheless, there is still much illegal activity that is funded through cryptographic techniques. Nearly 10% of the cryptocurrency exchanges are scams, and another 5% of failed crypto exchanges had their funds hijacked by massive hacks. Even supposedly ‘stable’ cryptocurrencies have failed after suffering wild swings in their value. Ransomware is still rampant throughout the business world, and the great majority of ransomware attacks demand payment in cryptocurrency to the hackers. Chainalysis estimates that firms paid some $350 million in ransom in 2020, and the amount of ransomware is believed to be increasing each year. It is also the case that even when authorities are able to track down the perpetrators of these crimes, they may not be able to bring the culprits to justice if they are located in countries such as Russia or North Korea. The Russians appear to tolerate hackers as long as they do not attack targets inside Russia, while the North Korean hackers appear to be part of Kim Jong-un’s government.

One of the most infamous ransomware attacks was the 2017 WannaCry attack. It infected as many as 300,000 PCs around the world. It was discovered that this ransomware attack used an exploit called EternalBlue to break into the computers. This exploit had been discovered by the US National Security Agency; however the NSA had not notified Microsoft of its existence. A month before this attack, a group called the Shadow Brokers stole the EternalBlue exploit and leaked it. Shortly before the WannaCry ransomware attack, Microsoft had issued a patch that protected computers from EternalBlue. However, many computer owners had failed to install the patch, and older computers had not received the patch from Microsoft. Hours after the WannaCry ransomware attack, a “kill switch” was created and installed. This protected computers that were already infected from being encrypted or from spreading the program to other computers. Worldwide, it is estimated that 300,000 computers were infected, and that it caused hundreds of millions or billions of dollars in damage and ransom. The attackers demanded ransom payments in Bitcoin. In Dec. 2017, the U.S. and U.K. announced that the attack originated from North Korea.

Figure V.7: A screen grab of the message received by recipients of the WannaCry ransomware attack of 2017.

So, what will happen to cryptocurrency and blockchain technology in the future? In this review we have limited our focus to the public blockchain. However, it is also possible for groups to utilize private blockchains; in this case it is far more difficult to follow the path of funds. There are also more recent cryptocurrencies that use techniques designed to thwart efforts to track transactions through the blockchain. One of these, Monero, “mixes” every transaction with other transactions, and utilizes other techniques that make it more difficult to trace money as it makes its way through the blockchain. A newer cryptocurrency, ZCash, uses a feature called “shielded transactions.” This feature insures that transactions using ZCash are “provably inaccessible.” Patrons who use ZCash are guaranteed anonymity. However, to date the fractions of transactions that use Monero or ZCash are extremely small relative to those in the dominant currencies Bitcoin and ETH.

Chainalysis founder Matthew Gronager predicts that blockchain technology users and law enforcement agencies will be engaged in a “cat-and-mouse game” throughout the future. Computer specialists and cryptographers will be constantly attempting to shield transactions from scrutiny, using more and more tools to protect the users’ privacy, while government agencies will search for new and more effective means to identify users and their transactions.

So what is the future of cryptocurrency? It appears that cryptocurrency has gained a sufficient foothold in the world economic system that it will not completely fail. New York Times reporter David Segal recently interviewed a number of cryptocurrency advocates and found that they were remarkably upbeat about the future prospects for crypto. Today, cryptocurrency is widely used by investors as an alternative or supplement to traditional investments. We have also shown that in certain areas, particularly online gaming, cryptocurrency is widely used and has some advantages in producing ‘provably fair’ gaming.

One scenario is that the recent cryptocurrency setbacks are temporary, and that crypto will once again see a dramatic increase in value and begin to be more widely accepted in the world of commerce. For this scenario to occur, it would seem that the field needs regulation to prevent scams, frauds and hacks. Already, financial regulatory bodies in many countries have required cryptocurrency exchanges, stablecoin issuers, and non-fungible token marketplaces to adopt anti-money laundering (AML) and know-your-customer (KYC) protocols. In the US, these regulations are imposed by the Bank Secrecy Act originally passed by Congress in 1970 and enforced by the Financial Crimes Enforcement Network (FinCEN) within the Treasury Department. Furthermore, the bipartisan infrastructure law passed by Congress and signed by President Biden in 2021 requires cryptocurrency brokers to report any digital-asset transfer moved to an account of an unknown person or address. These regulations are intended to make money laundering less profitable and more risky through continuous monitoring of crypto transactions for suspicious activity, and to provide user identity verification procedures to facilitate law enforcement investigations to prosecute financial crimes. If the field is to be more strongly regulated to provide stability and security, the logical candidates to oversee these regulations are the large banking and investment institutions. However, if this is the case, cryptocurrencies could well lose their status as outside disrupters of the economic order, and instead become embedded in our traditional commercial structure.

It is also increasingly likely that most governments will adopt stronger regulations restricting crypto transactions. One example is a “travel rule” for “minimizing the anonymity of large cryptocurrency transactions” by mandating that virtual asset service providers (VASPs) “obtain, hold and exchange information about the originators and beneficiaries of cryptocurrency transfers with other VASPs and above a certain threshold.” FinCEN has proposed a threshold of only $250 worth of crypto assets. In addition, the US Treasury Department has recommended that stablecoin issuers “be regulated like banks, with reserve and reporting requirements to match.” Government regulations are intended not only to prevent financial crimes, but also to generate appropriate tax revenue from digital currencies. Most countries, including the U.S. and U.K. treat cryptocurrencies not as legal tender, but rather as property akin to stocks and real estate, and subjected like those asset classes to capital gains, state and federal income taxes.

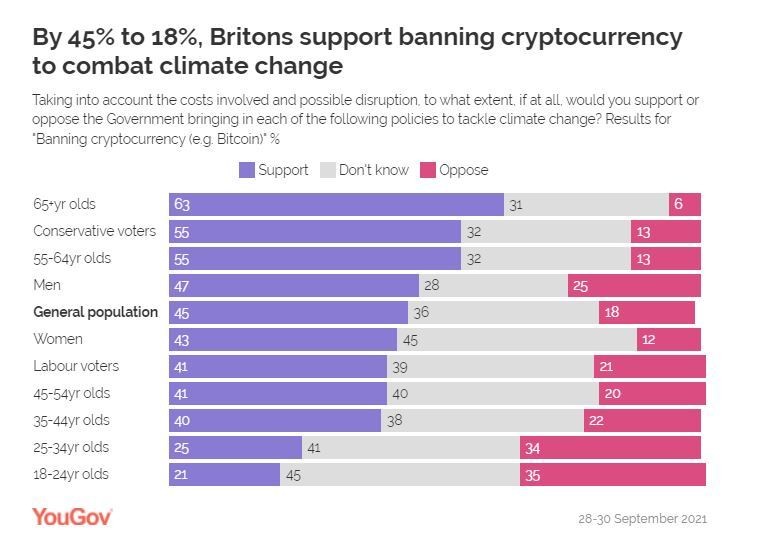

Of course, the ultimate government regulation that could be considered in some countries is a total ban on cryptocurrency transactions. Such bans are now in effect in China and eight other countries. In India, the Ministry of Finance equated cryptocurrencies to Ponzi schemes and the Royal Bank of India banned cryptocurrency activity entirely in 2018. However, the Indian Supreme Court struck down the ban in 2020, and now India has an adoption rate similar to that of the U.S. (see Fig. V.6). In the U.K., the poll results shown in Fig. V.8 reveal pretty strong public support, especially among seniors, for banning cryptocurrency (presumably, only those currencies that use proof-of-work protocols for the blockchain) as part of a plan for combating climate change. Even falling short of complete bans, however, increased government regulation will bring the crypto ecosystem still further away from the original naïve dream of cypherpunks and crypto-anarchists to create a financial system completely independent of and invisible to governments and traditional financial institutions.

Another possibility is that cryptocurrency will continue to experience radical swings in volatility, and that hacks, frauds and scams will continue for some time. At the moment (Feb. 2023), the value of Bitcoin seems to have bottomed and then shown a slight increase. This has occurred immediately following the shocking revelations of widespread fraud in the cryptocurrency exchange FTX. FTX was not only the largest crypto exchange, but it had sponsored a number of commercials by celebrity endorsers such as Tom Brady, Gisele Bundchen, Stephen Curry, Shaquille O’Neal, Shohei Ohtani, Naomi Osaka and Larry David. A number of class-action suits have been filed against these figures for promoting FTX immediately before it crashed amidst allegations of widespread fraud. However, Kevin O’Leary of the TV show ‘Shark Tank’ claims with ‘100% certainty’ that cryptocurrency tokens will suffer “meltdown to zero” on a regular basis.

This post has focused on what are called public blockchains; in these systems, the blockchain is visible to anyone and a combination of public and private keys are used to provide pseudonymity to users. However, a number of banking and investment firms have begun using private blockchains to manage their inventory and keep records of transactions. It may well turn out that private blockchains represent the future of cryptographic techniques in business. If this is the case, then the cryptographic methods will no longer be disrupting to traditional business – these traditional businesses may use blockchain technology as part of their regular banking, legal or commercial businesses. It remains the case that the use of cryptography in transactions has enormous potential. We will see whether a system can be created where cryptocurrencies are stable, secure and widely accepted. We will also see how governments decide to regulate industries that utilize these techniques.

Source Material:

Wikipedia, Collapse of FTX, https://en.wikipedia.org/wiki/Bankruptcy_of_FTX

Wikipedia Cypherpunks https://en.wikipedia.org/wiki/Cypherpunk

Wikipedia Data Encryption Standard https://en.wikipedia.org/wiki/Data_Encryption_Standard

W. Diffie and M. Hellman, “New Directions in Cryptography” (PDF). IEEE Transactions on Information Theory. 22 (6): 644–654. https://ee.stanford.edu/~hellman/publications/24.pdf

Andy Greenberg, Tracers in the Dark: The Global Hunt for the Crime Lords of Cryptocurrency, Doubleday 2022, https://www.amazon.com/Tracers-Dark-Global-Crime-Cryptocurrency/dp/0385548095/

Timothy May, The Crypto Anarchist Manifesto, https://groups.csail.mit.edu/mac/classes/6.805/articles/crypto/cypherpunks/may-crypto-manifesto.html

Wikipedia, Satoshi Nakamoto https://en.wikipedia.org/wiki/Satoshi_Nakamoto

‘Newsweek’ Says it Found Bitcoin’s Founder: 4 Things to Know, Emily Siner, NPR.org, Mar. 6, 2014 https://www.npr.org/sections/alltechconsidered/2014/03/06/286833324/4-things-to-take-away-from-newsweek-s-report-on-the-founder-of-bitcoin

Satoshi Nakamoto, Bitcoin: A Peer-to-Peer Electronic Cash System, white paper Oct 31, 2008 https://bitcoin.org/bitcoin.pdf

Wikipedia, Nick Szabo https://en.wikipedia.org/wiki/Nick_Szabo

Wikipedia, Hal Finney (computer scientist) https://en.wikipedia.org/wiki/Hal_Finney_(computer_scientist)

Wikipedia Craig Steven Wright https://en.wikipedia.org/wiki/Craig_Steven_Wright

Wikipedia, Sam Bankman-Fried https://en.wikipedia.org/wiki/Sam_Bankman-Fried

FTX’s New CEO, John Ray, Details Crypto Exchange’s Downfall in US House Testimony, Jaquelyn Melinek, TechCrunch.com, Dec. 13, 2022 https://techcrunch.com/2022/12/13/ftxs-new-ceo-john-ray-details-crypto-exchanges-downfall-in-us-house-testimony/

Wikipedia, Changpeng Zhao https://en.wikipedia.org/wiki/Changpeng_Zhao

The Basics of Bitcoins and Blockchains: An Introduction to Cryptocurrencies and the Technology That Powers Them, by Antony Lewis, Mango 2018 https://www.amazon.com/Basics-Bitcoins-Blockchains-Introduction-Cryptocurrencies/dp/1633538001

Wikipedia, Cryptographic Hash Functions https://en.wikipedia.org/wiki/Cryptographic_hash_function

Wikipedia, Secure Hash Algorithms https://en.wikipedia.org/wiki/Secure_Hash_Algorithms

Bitcoin Halving, Explained, CoinDesk.com https://www.coindesk.com/learn/bitcoin-halving-explained/

Wikipedia, Ethereum https://en.wikipedia.org/wiki/Ethereum

Wikipedia, Non-fungible Token https://en.wikipedia.org/wiki/Non-fungible_token

Gavin Wood, Ethereum: A Secure Decentralized Generalised Transaction Ledger, yellowpaper. https://web.archive.org/web/20180203110042/http://yellowpaper.io/

Wikipedia, Smart Contract https://en.wikipedia.org/wiki/Smart_contract

R. Sharma, What Is Decentralized Finance (DeFi) and How Does it Work?, Investopedia.com, Sept. 21, 2022 https://www.investopedia.com/decentralized-finance-defi-5113835

CoinDesk.com, China Crypto Bans: A Complete History, Andrey Sergeenkov, Mar 9, 2022 https://www.coindesk.com/learn/china-crypto-bans-a-complete-history/

Wikipedia Proof of stake https://en.wikipedia.org/wiki/Proof_of_stake

Wikipedia, Byzantine fault https://en.wikipedia.org/wiki/Byzantine_fault

S. Meiklejohn et al., A Fistful of Bitcoins: Characterizing Payments Among Men With No Names, Communications of the ACM 59, p. 86 (2016) https://cacm.acm.org/magazines/2016/4/200174-a-fistful-of-bitcoins/abstract

Nick Bilton, American Kingpin: The Epic Hunt for the Criminal Mastermind Behind the Silk Road, Portfolio 2017. https://www.amazon.com/American-Kingpin-Catching-Billion-Dollar-Paperback/dp/0753546671/

Wikipedia Silk Road (marketplace) https://en.wikipedia.org/wiki/Silk_Road_(marketplace)

Andy Greenberg, The FBI Finally Says How it ‘Legally’ Pinpointed Silk Road’s Server, Wired.com Sept. 5 2014 https://www.wired.com/2014/09/the-fbi-finally-says-how-it-legally-pinpointed-silk-roads-server/

Corrupt Silk Road Agent Carl Force Sentenced to 78 Months, Joe Mullin, ArsTechnica.com, Oct. 19, 2015 https://arstechnica.com/tech-policy/2015/10/corrupt-silk-road-agent-carl-force-sentenced-to-78-months/

After Admitting to New Crime, Ex-Secret Service Agent Sentenced to 2 Years, Cyrus Farivar, ArsTechnica.com, Nov. 7, 2017 https://arstechnica.com/tech-policy/2017/11/ex-agent-corrupted-by-silk-road-sentenced-to-2-additional-years/

Chainalysis: The Blockchain Data Platform https://www.chainalysis.com/

The Tor Project, https://www.torproject.org/

Yashu Gola, What BTC Price Slump? Bitcoin Outperforms Stocks and Gold for 3rd Year in a Row, Cointelegraph.com, Dec. 29, 2021 https://cointelegraph.com/news/what-btc-price-slump-bitcoin-outperforms-stocks-and-gold-for-3rd-year-in-a-row

Dead Coins, Cryptocurrencies Forgotten by This World, https://99Bitcoins.com/deadcoins

Wikipedia Mt. Gox https://en.wikipedia.org/wiki/Mt._Gox

Reported Crypto Scam Losses Since 2021 top $1 Billion, Says FTC Data Spotlight; Leslie Fair, FTC.gov, June 3, 2022 https://www.ftc.gov/business-guidance/blog/2022/06/reported-crypto-scam-losses-2021-top-1-billion-says-ftc-data-spotlight

Crypto Hackers Stole Almost $2 Billion in H1 2022, July 11 2022, Crypto World Network News, July 11, 2022 https://www.cw-nn.com/crypto-hackers-stole-almost-2-billion-in-h1-2022/

Chainalysis Company Information, Funding & Investors, Dealroom.co https://app.dealroom.co/companies/chainalysis

How Provably Fair Gambling With Bitcoin Works, Audrey Weston Nov. 16 2022 https://www.gamblingsites.com/bitcoin/provably-fair-gambling/

B. Jones, A. Goodkind and R. Berrens, Economic Estimation of Bitcoin Mining’s Climate Damages Demonstrates Closer Resemblance to Digital Crude Than Digital Gold, Nature Scientific Reports 12, 14512 (2022). https://www.nature.com/articles/s41598-022-18686-8

Wikipedia WannaCry ransomware attack https://en.wikipedia.org/wiki/WannaCry_ransomware_attack

Crypto Meltdown, What Crypto Meltdown? David Segal, New York Times, Jan. 17 2023 https://www.nytimes.com/2023/01/17/business/crypto-market-meltdown-nft-blockchain.html

Kevin O’Leary Warns Another Crypto ‘Meltdown to Zero’ Will 100% Happen, Paul L., Finbold News, Jan. 17, 2023 https://finbold.com/kevin-oleary-warns-another-crypto-meltdown-to-zero-will-100-happen/

Celebrity Crypto Ambassadors Sued Over FTX Crash, Zoe Guy, Vulture, Nov. 17, 2022 https://www.vulture.com/2022/11/ftx-lawsuit-celebrities.html

The Crypto Ponzi Scheme Avenger, David Segal, New York Times Nov 11, 2022 https://www.nytimes.com/2022/11/11/business/crypto-ponzi-scheme-hyperfund.html

The Crypto World is on Edge After a String of Hacks, David Yaffe-Bellany, New York Times, Sept 28, 2022 https://www.nytimes.com/2022/09/28/technology/crypto-hacks-defi.html

Coinbase Reaches $100 Million Settlement With New York Regulators; Matthew Goldstein and Emily Flitter, New York Times, Jan 4 2023 https://www.nytimes.com/2023/01/04/business/coinbase-settlement-anti-money-laundering.html

Since 2014, Roughly 42% of Failed Crypto Exchanges Have Disappeared Without a Trace for No Apparent Reason, Jamie Redman, Bitcoin.com July 25, 2022 https://news.bitcoin.com/since-2014-roughly-42-of-failed-crypto-exchanges-have-disappeared-without-a-trace-for-no-apparent-reason/

Reported Crypto Scam Losses Since 2021 top $1 Billion, Says FTC Data Spotlight; Leslie Fair, FTC.gov, June 3 2022 https://www.ftc.gov/business-guidance/blog/2022/06/reported-crypto-scam-losses-2021-top-1-billion-says-ftc-data-spotlight

M. DeCambre, Who Owns Bitcoin? Roughly 80% are Held by Long-Term Investors: Report, MarketWatch, Feb. 11, 2021, https://www.marketwatch.com/story/who-owns-bitcoin-roughly-80-are-held-by-long-term-investors-report-11612998740

@cryptovest, Bitcoin and Blockchain: What Math Puzzle Do Miners Actually Solve? Example with Real Transactions, https://steemit.com/bitcoin/@cryptovest/bitcoin-and-blockchain-what-math-puzzle-do-miners-actually-solve

Chainalysis Team, How Governments Regulate Cryptocurrency, https://blog.chainalysis.com/reports/cryptocurrency-regulation-explained/

J. Edwards, Bitcoin’s Price History, Investopedia, Dec. 20, 2022, https://www.investopedia.com/articles/forex/121815/bitcoins-price-history.asp

Environmental Effects of Bitcoin, Wikipedia, https://en.wikipedia.org/wiki/Environmental_effects_of_Bitcoin

Cambridge Bitcoin Electricity Consumption Index

L. Daly, What is Proof-of-Stake (PoS) in Crypto?, The Motley Fool, Dec. 12, 2022, https://www.fool.com/investing/stock-market/market-sectors/financials/cryptocurrency-stocks/proof-of-stake/

Chainalysis Team, Cryptocurrency Ecosystem Comparison: Bitcoin vs. Ethereum vs. Stablecoins, July 1, 2021, https://blog.chainalysis.com/reports/cryptocurrency-ecosystem-bitcoin-ethereum-stablecoins/

L. Daly, How Many Cryptocurrencies Are There?, The Motley Fool, June 27, 2022, https://www.fool.com/investing/stock-market/market-sectors/financials/cryptocurrency-stocks/how-many-cryptocurrencies-are-there/

Chainalysis Team, Crypto Crime Trends for 2022: Illicit Transaction Activity Reaches All-Time High in Value, All-Time Low in Share of All Cryptocurrency Activity, Jan. 6, 2022, https://blog.chainalysis.com/reports/2022-crypto-crime-report-introduction/

Chainalysis Team, Darknet Market Activity Higher Than Ever in 2019 Despite Closures. How Does Law Enforcement Respond?, Jan. 28, 2020, https://blog.chainalysis.com/reports/darknet-markets-cryptocurrency-2019/

Chainalysis Team, How Darknet Markets and Fraud Shops Fought for Users In the Wake of Hydra’s Collapse, Feb. 9, 2023, https://blog.chainalysis.com/reports/how-darknet-markets-fought-for-users-in-wake-of-hydra-collapse-2022/

https://dnstats.net/site/silk-road-3-1/

R. Bellan, Tesla Records $204M Loss from Bitcoin in 2022, TechCrunch, Jan. 31, 2023, https://techcrunch.com/2023/01/31/tesla-records-204m-loss-from-bitcoin-in-2022/

Wikipedia, Stablecoin, https://en.wikipedia.org/wiki/Stablecoin

E. Wolff-Mann, ‘Only Good for Drug Dealers’: More Nobel Prize Winners Snub Bitcoin, Yahoo Finance, Apr. 27, 2018, https://finance.yahoo.com/news/good-drug-dealers-nobel-prize-winners-snub-bitcoin-184903784.html

Wikipedia, Tulip Mania, https://en.wikipedia.org/wiki/Tulip_mania

S. Kemp, Digital 2022: Big Rise in Cryptocurrency Ownership, DataReportal, Jan. 26, 2022, https://datareportal.com/reports/digital-2022-big-rise-in-cryptocurrency-ownership

A. Goldberg, W. Sheridan, and Y. Kunihira-Davidson, What the US Infrastructure Bill Means for Cryptocurrency Brokers and Owners, Part II, S&P Global Market Intelligence, Dec. 20, 2021, https://www.spglobal.com/marketintelligence/en/mi/research-analysis/what-the-us-infrastructure-bill-means-for-cryptocurrency-brokers-and-owners.html

Chainalysis Team, What is AML and KYC for Crypto?, Dec. 14, 2021, https://blog.chainalysis.com/reports/what-is-aml-and-kyc-for-crypto/

M. Quiroz-Gutierrez, Crypto is Fully Banned in China and 8 Other Countries, Fortune, Jan. 4, 2022, https://fortune.com/2022/01/04/crypto-banned-china-other-countries/

M. Smith, By 45% to 18%, Britons Support Banning Cryptocurrency to Combat Climate Change, YouGov Poll, Oct. 21, 2021, https://yougov.co.uk/topics/politics/articles-reports/2021/10/21/45-18-britons-support-banning-cryptocurrency-comba